Dunelm (LON: DNLM) - Full thesis

20 years of uninterrupted growth, 8-10% dividend yield, and a structural question about urban stores that determines whether this is a stalwart or a compounder.

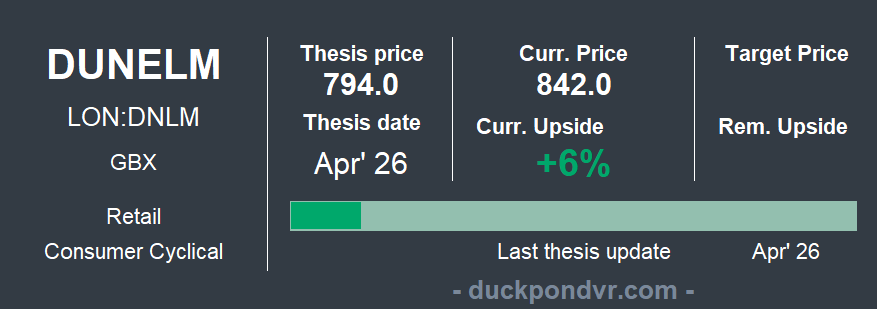

5 minute drill

Dunelm is the UK’s market leader retailer in homewares with over 200 stores. Still controlled by its founding family, the company delivered 20 years of sustained sales growth of 9% annualized (except 2020), sustaining operating margins above 12% and with a shareholder remuneration policy via dividend with payouts close to 100% and a very contained financial debt.

The company is currently trading at 10-11x earnings, averaging 15-16x, with a drop of more than 20% YTD, mainly due to two factors:

A profit warning after a weaker-than-expected Q2 (Black Friday and Christmas), where sales grew only 1.6% vs Q2 2025, leaving FY2026 earnings in the low range of guidance, with wages incremental costs.

Since the outbreak of the Iran conflict, the market has priced in a potential stagflation scenario in the UK economy that structurally harms discretionary consumption.

Beyond these short-term headwinds, Dunelm faces a genuine structural question in its growth model. Its superstore format in retail parks already covers 60% of the UK population within a 15-minute drive. The remaining addressable market sits in dense urban centres, where the company is experimenting with smaller urban store formats. This model carries meaningful operational risks and brings Dunelm into more direct competition with M&S Home, Next Home, and a growing Amazon.

Dunelm, due to its size and penetration, has acted as a secular consolidator in a highly atomised market such as homeware and furniture, where its ability to maintain low ranges at good prices, its own brand with good value for money, bargaining power with suppliers and low debt allows it to opportunistically face adverse scenarios and end up capturing market share from small fish in a market that is barely growing.

Over the past 10 years, the company has achieved organic growth, expanding at a rate of 5-6 openings per year (including M&A) while increasing its like-for-like sales, gaining market share year after year.

Some of the ingredients of success have been to incorporate furniture product ranges where its market share in some families has doubled, to develop an omnichannel system that already represents 40% of sales, and all this in scenarios of strong price competition, sustaining its margins.

During the inflationary crisis caused by the war in Ukraine, Dunelm was trading at around £7 at 10 times earnings. When the business model showed solvency and continued to gain market share, the stock bounced back to £12-13, offering returns (including dividends) close to 100%.

Then: Dunelm is a high-quality company, excellently managed and prepared for the challenges it must face.

If the company increases its store park in the low range of the guidance (5-10 stores), it would grow in sales at an annualized 4% until 2030. With sustained margins, the company would trade at a multiple of 8.5x versus an average of 15-16x.

Does the company currently deserve such a high output multiple?

The full thesis, valuation, sensitivity analysis and a live Excel model with every assumption exposed are available for paid subscribers. The same research I produce for family offices, now available here. If this is the kind of research you were looking for, this is the moment.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com