Semapa (LSI: SEM) — ~50% discount and a potential catalyst

Net cash + listed assets at ~50% discount and a potential takeover.

Good afternoon, dear reader.

This week I was reviewing the Q1 results of the company I am writing about today, looking mainly for clues about how management plans to deploy the cash following the sale of a business that unlocked part of the value.

From here, the question is not just about the investment’s upside, but about the opportunity cost of waiting. Any signal about the destination of that capital matters, because this is my largest holding.

The result: there are no explicit signals. But today I will explain why that may be, counterintuitively, the best signal of all.

Position disclosure: Semapa represents 12% of the portfolio I manage, top position. There have been no recent purchases. We added during the tariff crisis in April 2025. The annualised return on the investment including dividends is 30%.

Reminder: the annual subscription discount ($400/year) is open until May 31st. Link here.

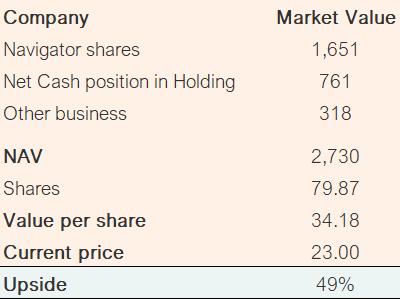

Semapa is a listed Portuguese holding company, owner of 70% of Europe’s largest paper company, Navigator Paper Company (ELI: NVG), among other businesses. One of them, Secil, a cement manufacturer primarily in the Iberian Peninsula, was sold at the end of 2025 for €1.08 billion. With the sale of Secil, the holding has moved from net debt to a net cash position of €761 million, equivalent to 40% of its current market capitalisation.

What will the company do with all that cash? No one can say for certain, but here are three clues:

Despite the cash position, the company has maintained last year’s dividend for the third consecutive year.

At the AGM on May 28th, a buyback programme covering 10% of shares will be voted on and approved.

In 2021, the controlling family attempted to take the company private.

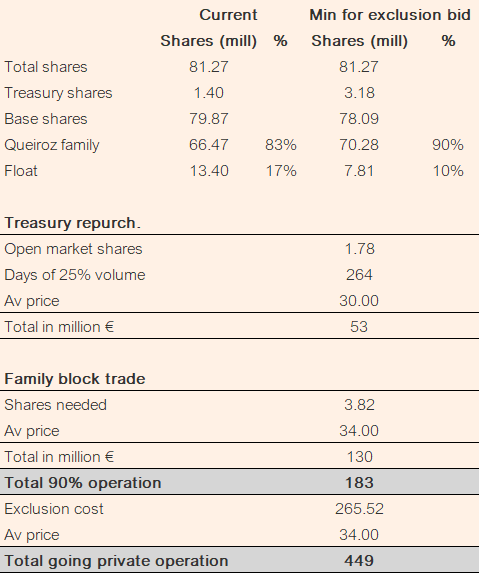

Currently, accounting for treasury shares (1.4 million shares), the Queiroz-Pereira family owns 83% of the company. If the buyback programme were executed in full, approximately 8 million shares, they would reach 93%, enough to launch a delisting bid. The problem is trading volume, which is below 30,000 shares per day. Buying 8 million shares in the open market is not realistic.

If the Queiroz-Pereira family wants to take the company private, we will have to witness a second round of what happened in 2021.

The failed 2021 takeover bid

In February 2021, the Queiroz-Pereira family launched, through its holding Sodim, a tender offer for Semapa’s free float. The initial price was €11.40 per share, a 20% premium over the previous day’s closing price. It was not enough. In April, Sodim raised the offer to €12.17 per share, a 6.8% increase, representing a total investment of approximately €277 million to acquire the ~28% they did not already control. It was still not enough.

The culprits, or the heroes, depending on who you ask, were four Spanish value managers: Bestinver, Cobas, Magallanes, and Horos, who refused to sell at the offered price, considering it too low.

The situation today is not the same: These funds have been waiting, just like myself, for years for the catalyst of this special situation, hoping the family would take the company private at a fairer price. The market has eventually rewarded that patience, but the remaining upside carries an opportunity cost: time.

The numbers

Taking into account the market price of Navigator shares, the net cash position of the holding, and the other businesses owned by Semapa, valued conservatively, the discount to NAV stands at 49%. A 30% discount if we value the non-listed businesses at zero.

*Navigator will be discussed below. It is a cost leader in a declining sector, and could reasonably be valued 20% above its current share price

While a holding discount would normally apply, in the context of a delisting bid we will use €34 as our reference price, anchored by cash and the market value of listed assets.

Open market purchases would take approximately 260 trading days, roughly one year, and the family would need to negotiate 3.8 million shares in block trades. The four musketeers from 2021, Cobas, Bestinver, Magallanes, and Horos, hold approximately 3.6 million shares between them.

The Queiroz family would need to deploy €130 million before securing the operation, and could fund the remaining €265 million through a special dividend.

The incentives exist: listing costs, regulatory compliance, and quarterly earnings pressure all disappear. The family has spent decades building an industrial empire, and maintaining a listed company with a 17% free float and barely 30,000 shares of daily volume provides neither fresh capital nor useful visibility. It only brings the scrutiny and deadlines of a public company without any of its advantages.

This is a real possibility, but not without risks.

Diworsification: the risk

In recent years the company has brought in investment banking professionals, and although small in scale, Semapa has acquired companies such as Triangle (bicycle frames) and Imedexa (energy services, high-voltage towers). The risk that they use this capital to buy more companies is real.

The market would not welcome such a move in the short term. Even if they eventually prove to be excellent serial acquirers, it would still be a holding company that is too diversified for a secondary European market.

Investing in declining industries

Investing in a declining industrial sector can be, counterintuitively, a very good idea. And Navigator, both via Semapa and directly, could be a great investment.

n the digital age, paper demand falls year after year. While office paper and textbooks (UWF) seem to have slowed their decline, newspaper and magazine paper consumption is now almost irrelevant (UME/CME). Who would want to invest in paper?

In a declining industry like this, you look for the last survivor. The low-cost producer. And that is Navigator. Beyond being Europe's largest producer, it benefits from having its forests vertically integrated with production.

In this sector, capital is not just scarce: capacity is actively closing. Falling demand is compounded by rising costs, including energy, and the difficulty of passing price increases through to customers.

In the last two years, 2.01 Mt of production has disappeared from the market. That is 12% of total European capacity:

2024 | Sappi (Belgium): -530,000 t

2024 | Sappi (Germany): -220,000 t

2024 | UPM (Germany): -610,000 t (two sites)

2025 | UPM (Germany): -270,000 t

2025 | Metsä Board (Finland): -210,000 t

2026 | Papresa (Spain): -375,000 t (bankruptcy)

2026 | Smurfit Westrock (UK): -200,000 t (proposed)

As capacity closes, Navigator’s pricing power increases. The company has already announced price increases of 4-7% for all UWF paper products sold in Europe, effective in April, with the upper end of the range applying to entry-level grades.

The sector also benefits from a natural transport moat A UWF paper reel can weigh 20-40 tonnes and, given its low unit cost, freight differentials above approximately 600 km by road begin to seriously erode margins. This provides meaningful protection in Navigator's core markets against lower-cost competitors located elsewhere in the world.

The company is shifting its investment focus away from traditional paper, growing its presence in Tissue and Packaging. It has recently announced a manufacturing agreement for Tissue products with Procter & Gamble.

Navigator is not a business anyone wants to own. That is precisely why it trades where it does. And that is precisely why, through Semapa, you can buy Europe’s lowest-cost paper producer at a 49% discount to NAV, with €761 million in net cash, a buyback programme approved this month, and a controlling family that has already tried to take the company private once.

The setup is unusual: a holding company nobody covers, in a sector nobody wants, with a catalyst nobody is pricing. That is the pond we fish in.

Thanks for reading the Value Pond 🦆. If you enjoyed it, don’t forget to leave a like 👍 subscribe 🖊 and share 🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com