the Pond Journal #10: Primark & Japan Screener

Bargains in Japan and a hidden giant in London.

Welcome to The Pond Journal #10, dear reader,

I’m happy to celebrate one month since The Value Pond became a paid publication. For those who are new: I publish institutional-grade research on companies I believe are genuinely mispriced. 7-9 full dossiers per year, Excel models, and complete position disclosure. Quality over quantity.

Reminder: the annual subscription discount ($400/year) is open until May 31st. Link here.

Today's five-minute read covers two things: Japan, a market full of overlooked bargains where I am sharing a free screener, and Primark's parent company, Associated British Foods.

Next in the Pond

Selecting a new company to analyse is always a complex process. I typically spend 2 to 5 hours on initial research before committing to a deeper dive. Most of the time, the decision to pass is almost immediate. This time I reached two conclusions:

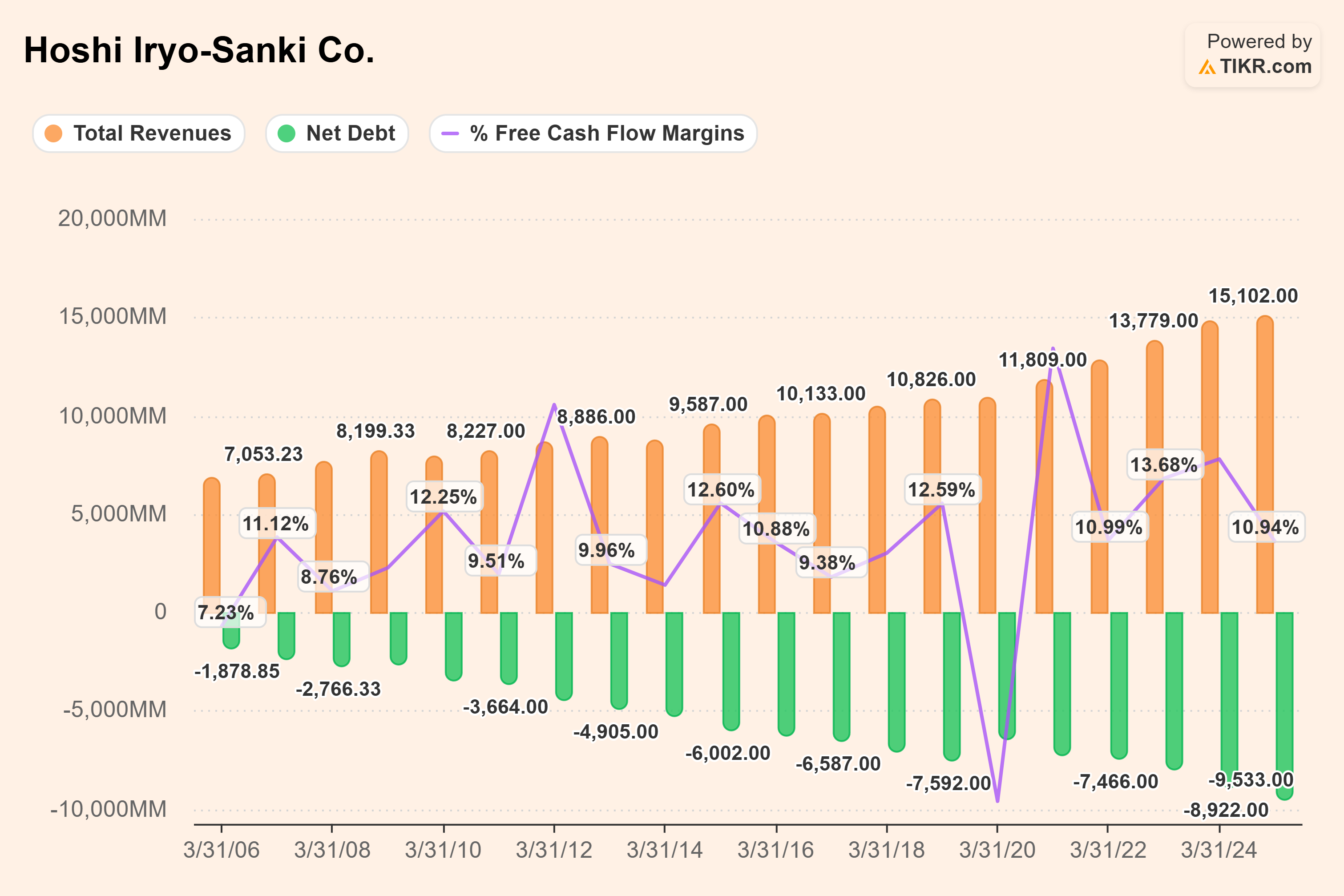

First: I want to analyse a Japanese small or mid cap, so I ran a mini-screener with very strict criteria: below 9x MC/FCF, below 1x Net Debt/EBITDA, FCF margins above 8%, EBIT margins above 10%, and trading below Book Value. Does this exist? Yes, it does.

I am sharing my own screener with 13 companies and updated metrics. The first one is a standout. I have not made a decision yet, but at least one of these 13 will end up in The Value Pond.

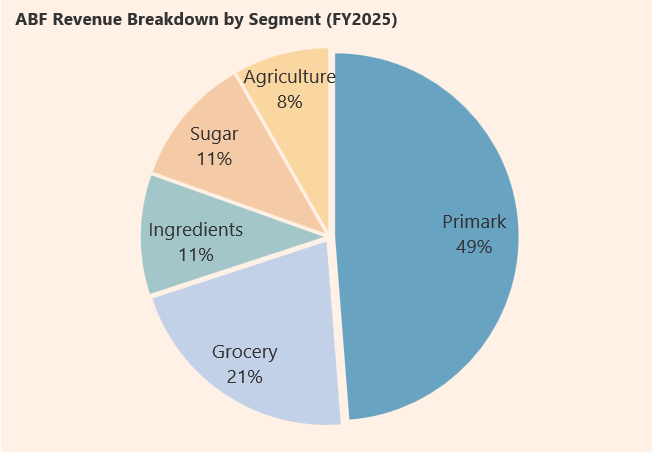

Second: While exploring the universe of announced spin-offs, I came across an old acquaintance: Associated British Foods. The British company may not ring a bell, but if I say Primark, it probably does. It is one of the giants of fashion retail.

Some of its consumer brands will also be familiar: Kingsmill, Silver Spoon, or Blue Dragon. Spanish readers will recognise Azucarera, also owned by ABF. And to all this is added an agricultural business.

In April 2026, the company announced it is planning a spin-off of the Primark brand, which represents 50% of group sales, to unlock its value and separate it from the rest of the business. The move makes sense.

If you value Primark at multiples comparable to Inditex or H&M, this segment alone supports 70% of ABF's current market capitalisation, leaving aside the other businesses that represent the remaining 50% of sales.

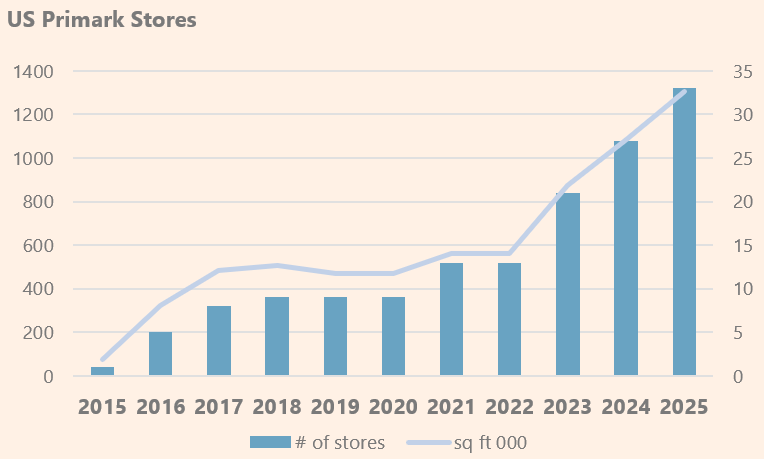

One of Primark's key growth vectors is the United States, where the brand has barely scratched the surface of its commercial expansion potential.

In summary, I believe Associated British Foods is a compelling sum-of-the-parts story, where it may be interesting to build a position even before the spin-off itself. But that is what the full thesis is for.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com