the Pond Journal #3

The Carnivorous Plants of Investing: Greenfire & the Incentive thread ⚠️

Welcome to the Pond Journal, a bimonthly newsletter fromDuckPond Value Research. In this third issue, we examine investment traps: one hidden inside a tempting deep-value play, and another lurking in everyday financial products.

I am hunting for value within the oil sector—we have discussed this in previous journals—and recently, a Canadian company crossed my radar: Greenfire Resources (TSX:GFR), which exploits bitumen deposits in Alberta, Canada. On paper, it looks like the perfect deep-value play: small, underfollowed and navigating temporary issues.

Even better, in 2024, the Waterous Energy Fund (WEF) acquired a majority stake and recently launched a rights offering. In this process, the fund has committed to subscribe to all shares that minority shareholders do not take up (effectively backstopping the issue). This move wipes out the company’s expensive debt (currently costing 8.5%).

By 2026, with normalized production and zero interest expense, Greenfire would trade at a P/E of ~6. With oil above $60/barrel, this looks like an easy 2x return or more. Sounds perfect, doesn’t it?

Pull the Thread of Incentives

Allow me to share a perfect example. A friend was recently offered an investment product by a traditional bank: a structured product which, over a five-year horizon, could pay a 6.5% annual coupon and return the principal, return only the principal, or result in capital loss, depending on the performance of the Euro Stoxx.

You read that right: capped upside, unlimited downside.

I told him to run away and apply a simple rule: “Pull the thread of incentives.” Are the seller’s incentives aligned with yours? Do they win when you win, or do they win simply by playing the game?

The Loaded Coin

If a stranger approaches you on the street with a coin and tells you that, in exchange for €10, he will pay you €50 if heads comes up at least 3 out of 10 times, the person proposing the game and setting the scenarios is playing with a loaded coin. There is a clear information asymmetry.

In the best-case scenario—which is quite probable given how it is structured—they will pay you a 6.5% coupon on the principal (from which a 7% upfront fee must be deducted). The result is an annualized return of 4.8%. I assure you, in this favorable scenario, the bank will make more off your money [than you will].

In the base case, they return the principal (minus fees), and you have effectively financed them for free for 5 years.

In the adverse scenario, the loss is unlimited and PERMANENT, since at maturity, the product ceases to exist. This is not a company that could recover its value over time.

One piece of advice, and let’s move on.

Avoid binary bets disguised as “guaranteed” products. Seek skin in the game. There are investment funds where the manager and their team have their entire personal net worth invested alongside yours. They win if you win; they lose if you lose.

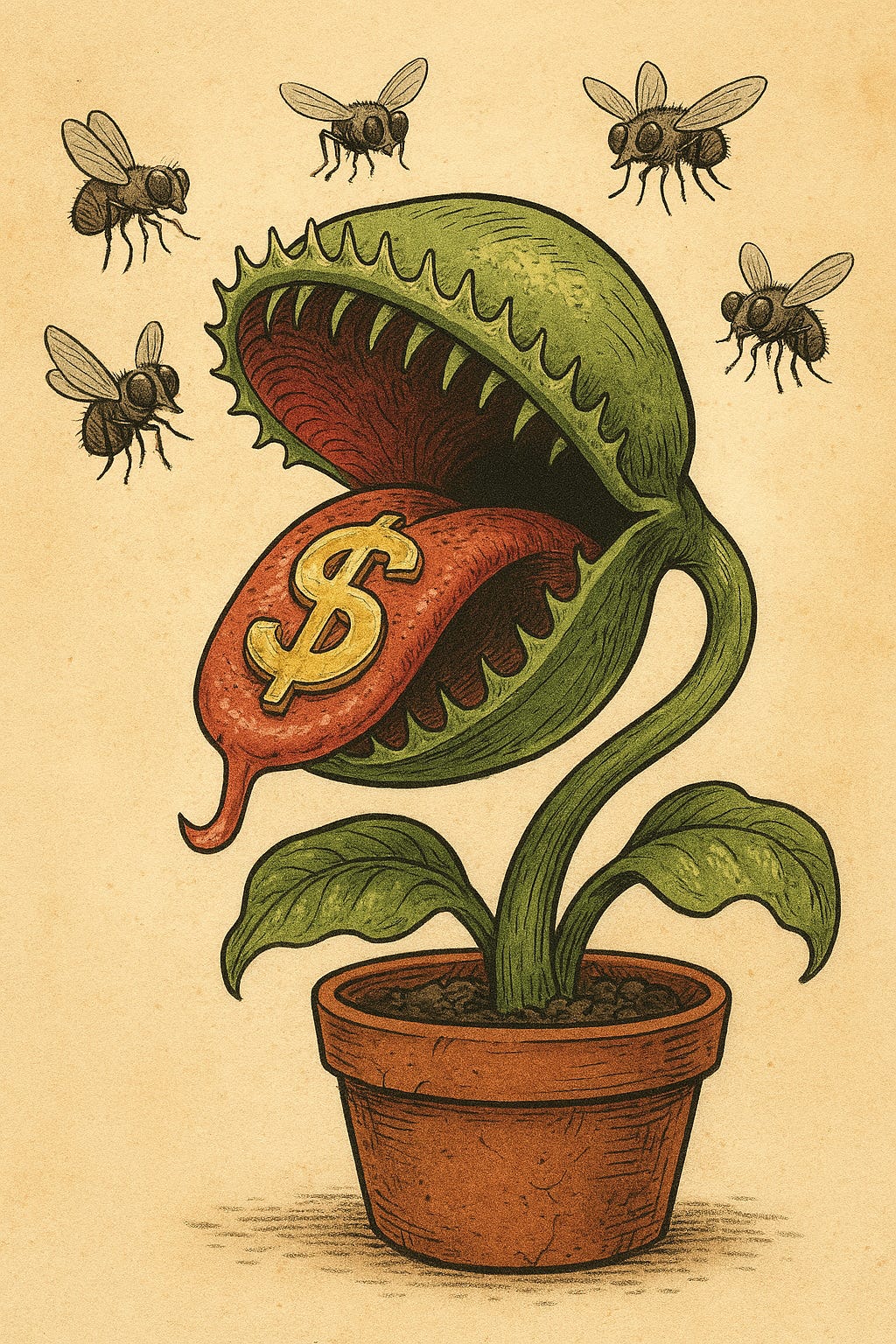

The Carnivorous Plant

Let’s revisit Greenfire Resources (TSX:GFR), the promising multibagger, to apply the two principles we discussed earlier: following the incentives and considering information asymmetry.

We saw that the majority shareholder (WEF) is willing to put up all the capital that minority shareholders do not contribute, in order to reduce the substantial debt load and financial expenses. Sounds fantastic. Let’s trace the line of incentives by investigating the track record of the Waterous Energy Fund:

In 2017, this fund began consolidating small and distressed assets in Canada, creating the company Strathcona. In late 2020, they launched a hostile takeover bid for a private company, Osum Oil Sands Corporation. It was initially rejected but finally approved in 2021 with a bid 25% higher, acquiring 87% of the share capital. Shortly after, having secured absolute control, they approved a merger with Strathcona, creating Strathcona Resources, and squeezed out the remaining minority shareholders of Osum at the same price as the accepted offer.

In 2023, they took Strathcona Resources (TSX:SCR) public on the Canadian exchange, and following subsequent mergers, it has become one of Canada’s large heavy crude producers. Strathcona is ~10 times larger than Greenfire itself in terms of daily barrel production.

The success of this producer consolidation strategy is evident and has delivered strong stock market performance. Furthermore, they recently divested ~7% of Strathcona Resources, raising approximately CAD 400–500 million, though they retain a stake of over 70%.

The playbook used with Osum Oil Sands is familiar territory for WEF, as they opted for a similar approach with Greenfire in 2024. They persuaded minority shareholders and, through a hostile takeover bid, wrested control from the previous owners, ousting the management team.

Waterous Energy Fund currently controls 60% of the company ( Q3 2025 Financial Statements), while the remaining shareholding is highly fragmented following the exit of the previous anchor shareholders.

Under Canadian law, a supermajority of 66⅔% of shareholder votes is required at the meeting. While WEF’s current stake falls slightly short, the pending rights offering—where WEF has committed to a backstop—changes the math. They only need 40% of minority shareholders not to subscribe to the offering for WEF’s stake to exceed 68%.

The risk for minority shareholders from that point on is clear: Osum 2.0. With the stock price depressed, WEF could merge Greenfire into Strathcona for pennies on the dollar. Let’s not forget that WEF owns 70% of it.

For Strathcona, Greenfire would be a sweet deal. Easy to integrate, debt-free, and cheap. Furthermore, in an article from this year, a WEF manager stated:

“It’s very difficult, in Canada, for small, subscale oil companies to be able to attract capital. By consolidating them together, we’ve been able to take advantage of operating cost synergies,” Waterous said of Strathcona. He sees similar acquisition opportunities for Greenfire in Athabasca, a region in Western Canada in which Strathcona isn’t present, he added.”

Who do you believe WEF’s incentives are aligned with: their own participants and clients, or Greenfire’s minority shareholders?

WEF is doing a magnificent job compounding capital for its investors. But in this scenario, Greenfire is the carnivorous plant. The cheap valuation is the nectar. And we are the fly.

Thanks for reading the Pond Journal👍. If you enjoyed it, don’t forget to subscribe and share your thoughts in the comments ⬇️

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com

For additional information and transparency, I am leaving the comment that people who know the company better than I do have made following this publication in X.

Please read carefully both, comment and my answer. And make your own due diligence, always.

https://x.com/AlfredMorrisCat/status/1991712842760720597?s=20