Welcome to The Pond Journal #7. I'm writing to you this Monday because something very interesting happened on Friday, something that deserves to be in the Journal before the markets open this week.

Remember Liberty Global? Is a complex telecommunications conglomerate and investment holding company geographically diversified across Europe. Known for its opportunistic capital management under John Malone, it focuses on high leverage, tax minimization, and aggressive share buybacks to unlock shareholder value.

A little over a year ago, I wrote a thesis alongside Investment Notes , primarily focused on taking advantage of a special situation involving the Sunrise spinoff, which was set to unlock the value of both the spin-off and Liberty itself.

The value catalyzed, though only on the Sunrise AG leg. In Liberty, there is still around ~70% upside. The funny thing is, this past Friday we saw a very strange market situation, which could be a precursor to further catalysts.

The Anomaly🤔

Liberty Global trades through three share classes: Class A (LBTYA) and Class B (LBTYB) carry voting rights, while Class C (LBTYK) has the same economic rights but no voting power.

Furthermore, there is a massive difference between Class A and B: Class A has one vote per share, whereas Class B has 10 votes per share. In short, the company is controlled through the ownership of Class B shares.

These shares have historically been held by John Malone, the “Cable Cowboy”, and Mike Fries, his right-hand man and successor. Together, they hold ~90% of the Class B shares. This makes Class B highly illiquid, with an average daily volume of just over 1,000 shares, compared to the 3 million shares traded in the other two classes.

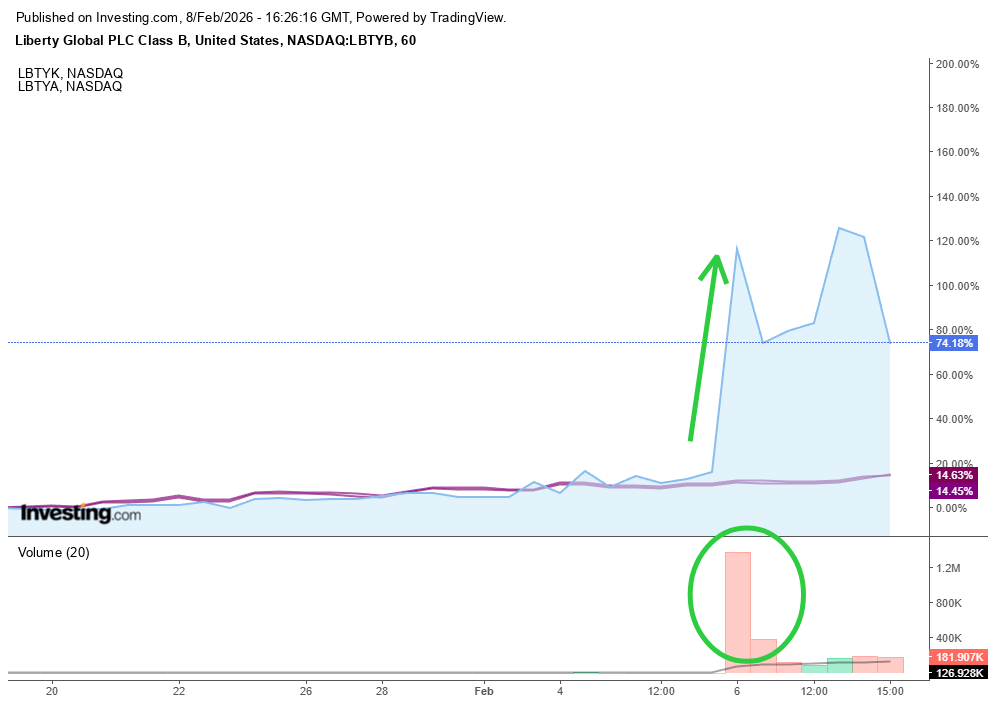

Usually, all three classes trade at parity. Until Friday.

Class B shares skyrocketed +100% at the open, hitting $29, while the other two classes remained below $12

Some say this was a short squeeze; honestly, I don't think that theory holds water. Not only is the short interest in this stock practically non-existent (185 shares), but the volume traded during the session tells a different story.

Opening volume was very high, dismissing the idea of sharp price swings on low liquidity: 1.2 million shares were traded against an average of 1,000 shares, with another 1.3 million shares moving throughout the day. This means ~19% of all Class B shares moved. In other words, 8% of the company's control votes changed hands at a roughly 50% premium.

And that, my friends, is no small feat.

The contagion reached Class A shares (1 vote per share), which saw their average volume double to 5.5 million shares, ending the day up 4%.

The company has up to four business days to report these moves to the SEC; only then will we know more. In the meantime, we can only speculate:

If we assume Malone/Fries haven't sold any of their Class B shares, someone has bet big on snatching up all other existing voting rights to take an active role in catalyzing the company's value.

If it’s Malone/Fries who have tightened their grip, something big is coming: A take-private bid? A simplification of share classes? Who knows.

Q4 2025 results will be presented this coming February 16th, and we also know that Fries/Malone are very fond of dropping major headlines the week before earnings.

Unreliable sources leaked on Friday that Liberty might be looking to acquire the 50% stake in the VodafoneZiggo joint venture (Netherlands) at an implied valuation of $4.40 billion, subsequently merging it with Telenet (their Belgian subsidiary) to create a Benelux giant. All speculation, nothing official.

What we do know is that Liberty Global is a clear case of undervaluation offering, in a conservative sum of the parts, a very attractive upside. These moves could stir the hornet's nest, forcing the actions needed to finally unlock that value. And if you have an undervalued stock in your sights, along with potential signs of upcoming catalysts, there is only one thing left to do.

An interesting week lies ahead after this strange event; I will be posting updates via X and Notes.

Thanks for reading the Pond Journal🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com