the Pond Journal #9

Geopolitics, market timing, and the only risk that really matters

Welcome to The Pond Journal #9, dear reader. A lot has happened in the Value Pond this past month, and a lot has happened in markets too.

The S&P500 closed last Friday at all-time highs. The Fear & Greed index sits at 68, firmly in Greed territory. The Eurostoxx50 is less than 1% from its own historical highs. All of this against a backdrop of a provisional ceasefire riddled with denials, reversals, and noise.

Trump has been playing a peculiar game with this war: agitating on Friday evenings post-close, then calming markets on Sunday pre-open: a juggling act designed to keep 20-year yields below 5%, oil below $100, and the impression that he is winning, winning fast, and conceding nothing. The Iranian regime is running a parallel game internally, but without internet, free press, or institutional/economical counterweights.

The closure of the Strait by the US, while dangerous, has changed the rules of the game by bringing China onto the board. China was among the countries most dependent on the Strait of Hormuz; in fact, the few ships allowed passage were bound for China, and the toll demanded by Iran was paid in Yuan or Bitcoin.

Polymarket has emerged as a 24/7 real-time thermometer, as interesting for reading global market sentiment as for watching the large players move. Right now, the most relevant variable for markets is the Strait of Hormuz, and its most perverse derivative: stagflation.

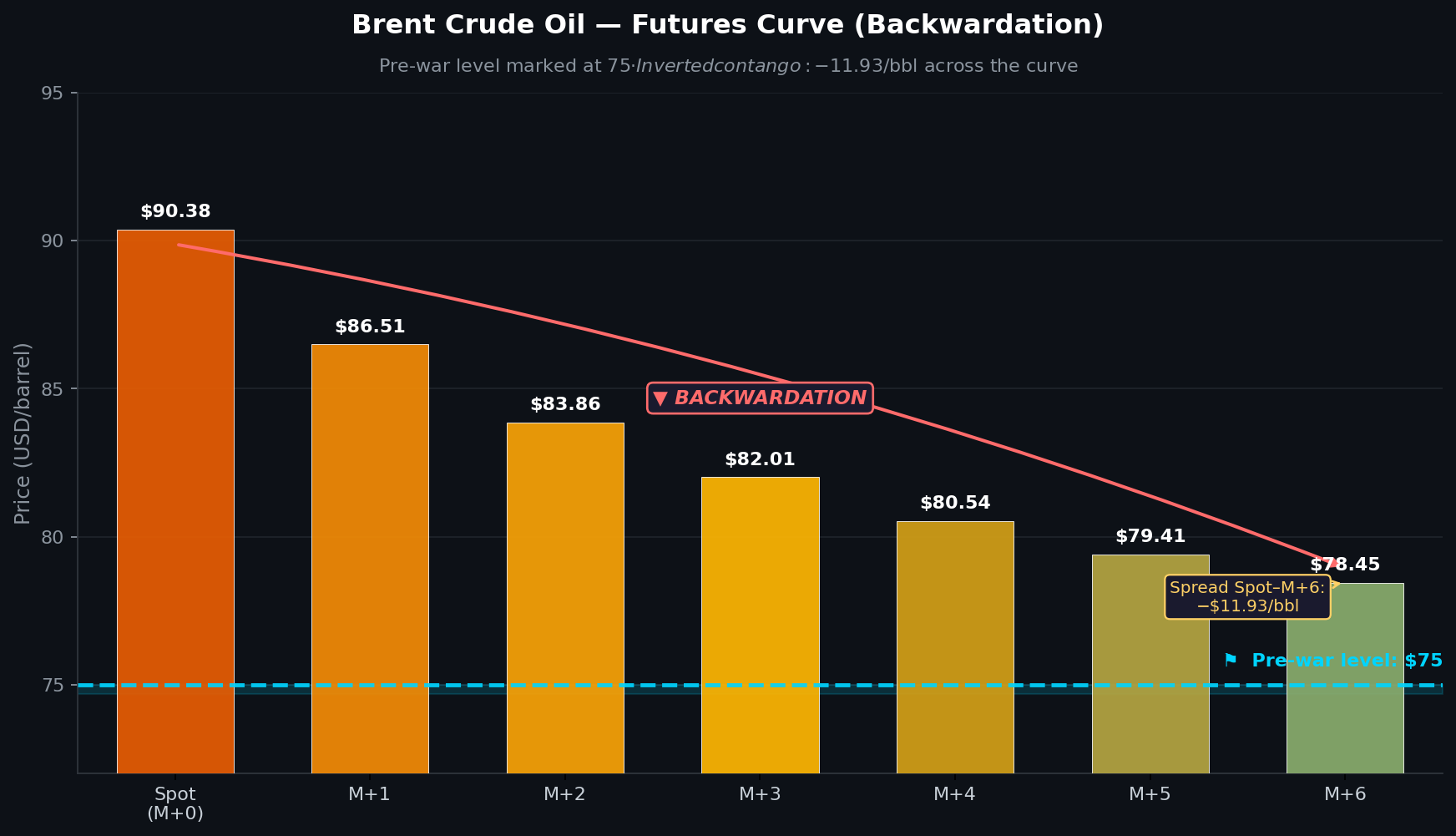

For its part, the Brent futures curve is already signaling a price only 5% higher for M+6. The market is pricing in this event as a temporary disruption that will eventually normalize. Probably there is too much euphoria for the amount of uncertainty still on the table.

Supply shocks have a cure: price incentives

When Russia invaded Ukraine, the narrative was apocalyptic. Ukraine was one of the world’s largest corn producers, a trigger for meat prices globally. Russian oil and gas supplied most of Europe. The end was near.

It wasn’t.

Supply shocks are painful in the short term. But they are also the most powerful incentive to develop resources elsewhere. Canada accelerated bitumen production. Offshore energy became economically viable again. In our Pond: Bayer was selling corn seeds & pesticides in the US & SA like never before. The same logic applies today.

Iran has shown it is willing to use the Strait as a weapon. But it may be a single-use weapon. Restoring passage through the strait and restoring confidence are two very different things. Gulf countries will seek alternatives and they will find them.

Short term, everyone suffers. Medium term, the economy reroutes.

The cost of being right about the wrong

Imagine you read the macro situation correctly one month ago. You saw the geopolitical risk, you decided to reduce exposure or exit entirely. Unless you have inside information from the Pentagon, you will likely have to stomach the initial, sharpest drop, where everything is uncertain.

Maybe this week was the perfect time to get back into the market. It seems like it’s all over. But what if it’s not? Do you exit again next week?

This is not a hypothetical. It happens to the most investors in the world. The problem with market timing is not that you cannot read the current situation, it is that you cannot read the future. No one knows where the bottom is. We only know that staying invested in good businesses at good prices has worked, consistently, across every crisis in modern history.

Buffett, Lynch, Howard Marks, none of them operated in calm waters. They operated through wars, hyperinflation, financial crises…. The lesson they all drew was the same. It is in moments like these that your conviction in what you’ve read is truly put to the test. It is one thing to read it; it is quite another to feel it.

The only question that matters is go through each position and ask one question: does this business have a future? could them survive? and embrace the volatility as an opportunity.

The risk you actually need to manage

There are two risks in investing:

The first is drawdown, your portfolio falls in value. This is painful but circumstantial. Markets recover. Good businesses recover faster.

The second is permanent capital loss, the business itself deteriorates. This is the one that cannot be undone. This is the risk worth obsessing over.

Trying to avoid both simultaneously is impossible. And trying to avoid the first by exiting the market usually just guarantees you miss the recovery.

We have all read the right books. Very few of us are capable of staying the course when it actually matters.

What’s new in the Pond

This past month has been the most active since The Value Pond launched. A few things worth flagging:

The blog has gone paid. Full institutional dossiers, live Excel models, and complete transparency on my own positions are now reserved for paid subscribers. The free tier keeps access to the 5-minute drill teaser for every thesis, plus articles like this one.

Three tiers are available. Paid subscriber at $500/year for the full research. Institutional subscriber at $1,500/year for everything above plus direct Q&A, priority on the research pipeline, and research on demand.

Two full theses are now live. Foraco (TSX:FAR) — a mining driller positioned for the commodity cycle and Dunelm (LON:DNLM) — the UK’s leading homewares retailer at 10-year PE lows with an 8-10% dividend yield.

Both include the full dossier and a live Excel model.

What’s next

A WizzAir update is coming. The original thesis was published in September 2025. With the stock back near those levels and new fuel price scenarios to model, an updated dossier with Excel model is in progress.

New full thesis expected around 20th May.

If any of this sounds like the kind of research you were looking for, the Pond is open.

Thanks for reading the Pond Journal🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com