Going Serious

Track Record, Proof of Work & What Comes Next

A few days ago, I announced that upcoming published theses will be behind a paywall. They will include a live Excel model and will follow an institutional dossier format. Hard financial drugs. (more info here). I also proposed a vote to select the first company to analyze. The vote is now closed with a tie. So i choose:

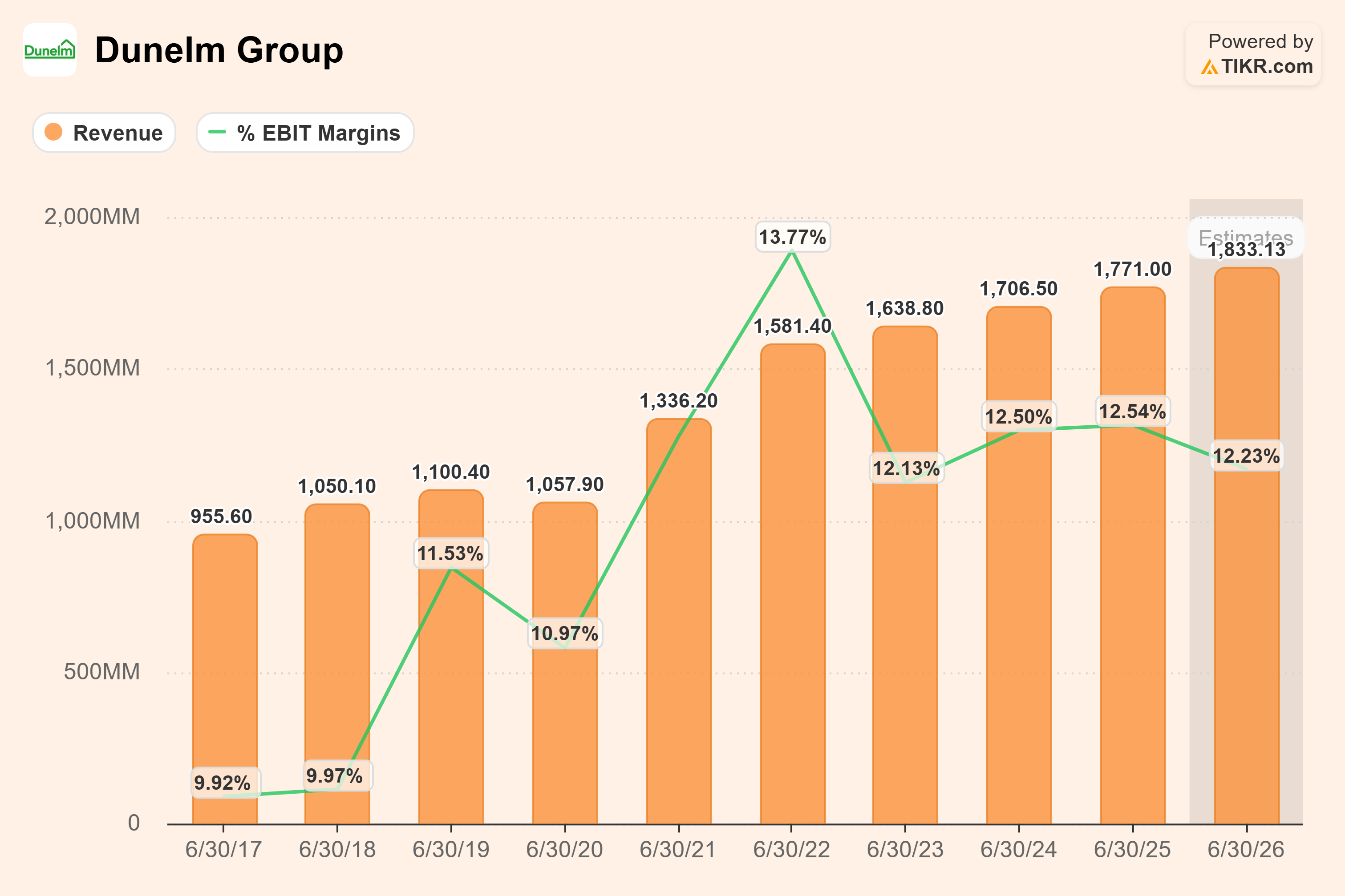

Dunelm Group (XLON: DNLM) — Specialty Retail | GBR A founder-led specialty retailer with a scalable business model, strong insider ownership, and consistent capital returns. In a sector often dismissed as structurally challenged. Dunelm stands out for the right reasons. I would not normally go after a business just because it is scalable, but it appears undervalued on first pass and carries contained debt.

Professional track-record

I am aware of the leap I am asking of my readers: yet another Substack going paid. I do not expect to reach 10,000 paying subscribers. But as I explained, that is not my game.

This is going to be niche. I am trying to scale something I already do for institutional clients, and they do not just want a well-documented thesis and an Excel model. They want to know your experience and your instinct.

Until now, I had never disclosed my annual returns. I only talked about specific companies. Why? A few reasons.

I never disclosed position sizing, entries or exits, so it felt unfair to talk about returns.

Some of my investments were theses never formalized on the blog, though I did mention them here or on X: IAG, Semapa, Flatex Degiro, Catalana Occidente, TGS….

Although my real track record goes further back, the demonstrable and most professional one starts on January 1st, 2023.

But now we are playing a different game, and the cards have to go on the table.

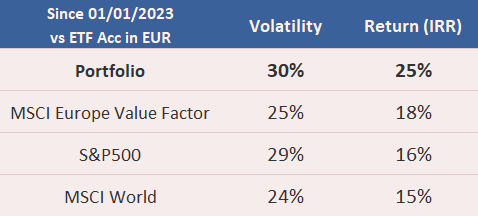

My current track record managing the family office stands at 25% annualized with 30% volatility (from 01/01/2023 to 03/27/2026). Note: I have absorbed a drawdown of more than 10% since the Iran conflict began.

What were the main drivers of this performance?

Concentration in 10-15 picks, overweighting 3-4 high-conviction ideas.

Margin of safety and long-term horizon.

Keeping liquidity to be aggressive during drawdowns.

Fishing for ideas in funds managed by people I trust.

Continuous learning.

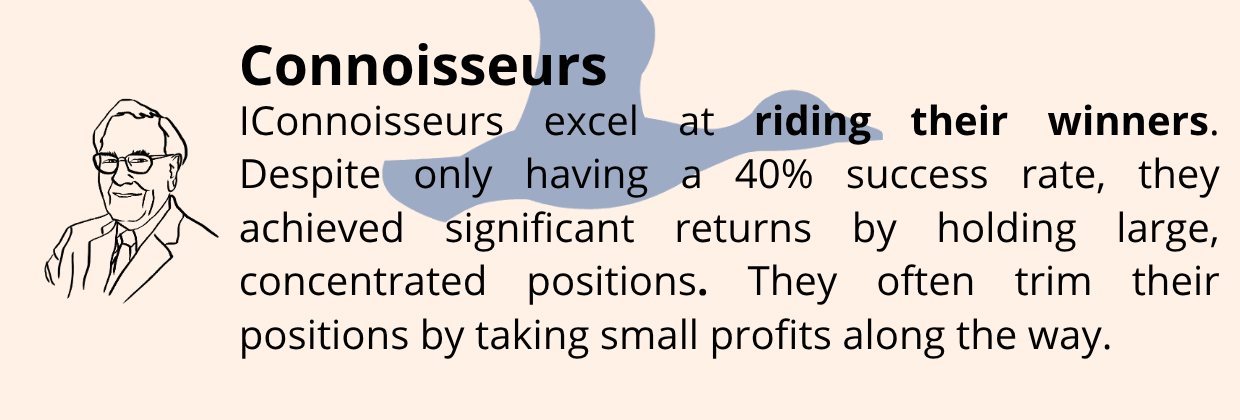

Acting as a Connoisseur.

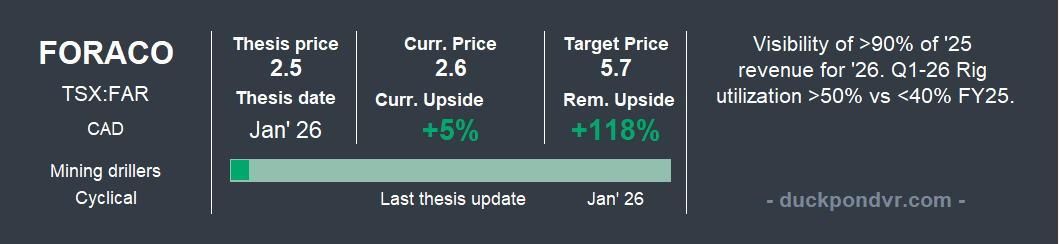

Foraco — Full Institutional Report

Beyond the upcoming Dunelm thesis, Foraco is a compelling reason to subscribe. It is one of my highest-conviction positions: the cycle is favorable, the thesis is resilient to the Iran conflict, the 2026 backlog guarantees strong visibility, and the CEO just bought shares. Full disclosure: it is my 4th largest position at 6% and I am currently adding.

I am making the full 14-page institutional report public — the one I produced for an institutional client, which complements the thesis I published here on Substack. The Excel model will be for paid subscribers only, at the bottom of this publication.

Thanks for reading the Pond Journal🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com