Forvia (FRA: FRVIA) - Update

Addition by Subtraction

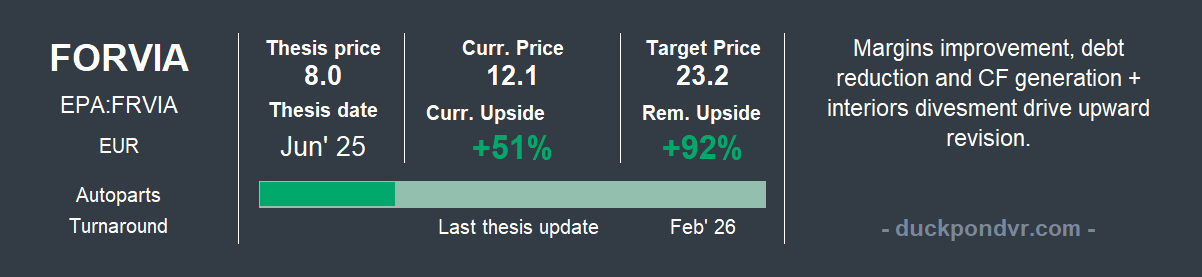

It has been less than a year since our original Forvia thesis, and the return since then is already over 50%. Granted, it’s taken a bit of a hit in the last few days, it had reached 80% at one point.

Forvia is boring; there’s no AI here, no glamorous product. Today, that very smell of metal and welding (asset-heavy) acts as a hedge against the AI-driven disruption currently shaking the markets. This is a pure industrial play: betting on a post-merger restructuring to boost margins and deleverage the balance sheet.

This is the kind of place where you come to roll up your sleeves and do the hard work. Even so, over 1,000 people stopped by to check it out. I’m leaving it here for you, as there are some details I won’t be revisiting today.

The 2025 results and the Capital Markets Day have brought a lot of new information to the table, enough to warrant a full review and a revision of the company’s price target. So, let’s get to it.

♟️Interiors: The Sacrificed Pawn.

The main and most critical piece of news is the sale of the Interiors division. Having been put up for sale in December, the deal is now considered a given for 2026. The impact on a company’s valuation when facing a divestment is a two-fold dilemma:

The earnings lost through the sale vs.

The debt reduction it enables.

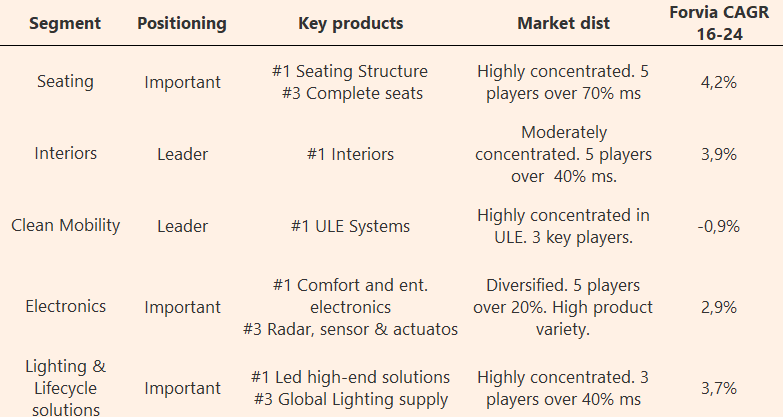

In these situations, the timing of the cycle and the urgency to sell heavily dictate the outcome. In Forvia’s case, the need for deleveraging is an undeniable fact. They are offloading a segment where they are a clear leader with a ~13% market share. Is this a negative? Let’s take a look 👁️.

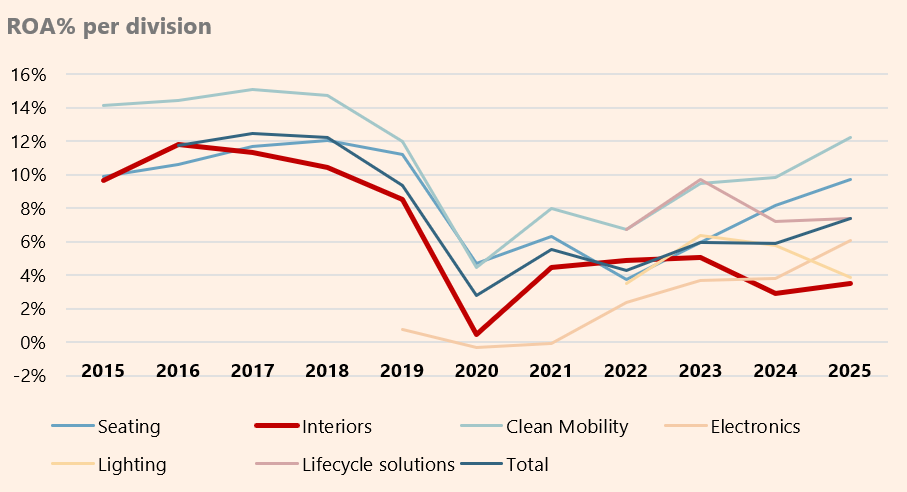

In the original thesis, we saw that Interiors was the division with the lowest Return on Assets (ROA) and the thinnest margins. Furthermore, after Lighting, it was consuming the highest level of CapEx relative to asset value, at around 4%.

Moreover, despite being a market leader, it is a lower value-added segment and is more fragmented among local competitors. We already touched upon this in the original thesis.

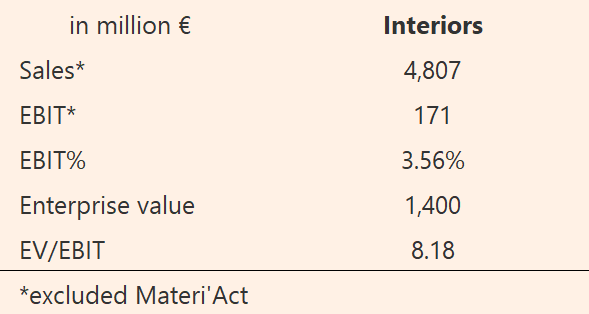

The expected Enterprise Value for the sale is estimated at approximately €1.4 billion—so much so that they have already adjusted the impairment loss against book value in the 2025 results.1 This valuation implies an EV/EBIT multiple of around 8x. This multiple is consistent with recent M&A transactions in the sector.

✅ Overall, the decision makes sense. The priority for unlocking value lies in improving margins and reducing debt. The Interiors division was the necessary sacrifice.

💼 Portfolio Redefinition

In its 2028 plan, Forvia has redefined the value proposition of its divisions by splitting them into two groups:

Growth Cluster: These are the divisions management considers growth drivers, where investment is truly worthwhile.

Value Cluster: Here, the priorities are margins and cash generation. This makes perfect sense.

I won’t dwell much longer on this topic. If you’d like to learn more about the strategy or the value proposition of each segment, you can consult the Forvia CMD 2026 Presentation.

💰Resultados 2025

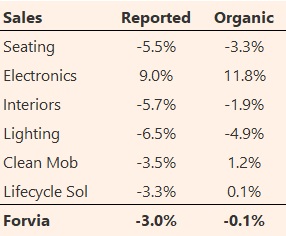

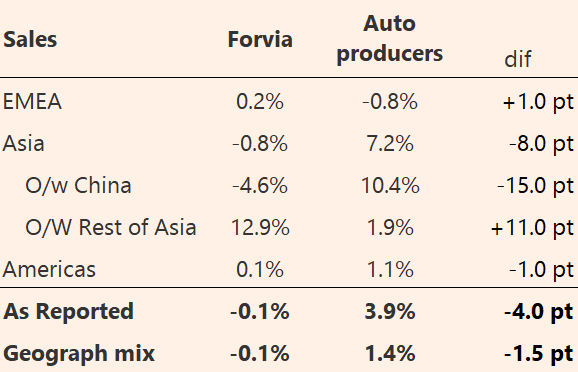

We knew top-line growth wouldn't set the world on fire, but we came here for an industrial restructuring play, not a compounder. Yet, they delivered exactly what was required: the guidance was met. Adjusted for currency, sales remained flat year-on-year. (If we include a “tooling” effect2 in Interiors, product sales actually grew by 1.5%).

When compared to global light vehicle production, which grew by 3.9%, Forvia lagged by 4 points. However, if we factor in Forvia’s specific geographic mix, production grew by 1.4%, representing a 1.5-point underperformance.

Chinese OEMs have entered a phase of offshoring production to Southeast Asian countries, and Forvia has been following them, to Thailand with BYD, for instance. Nonetheless, the net effect in Asia remains negative. This will need to be monitored closely.

We’ll discuss specific divisional sales later, but since the two pillars of this thesis are margin improvement and deleveraging, let’s see how they performed.

🔎Margins & Debt

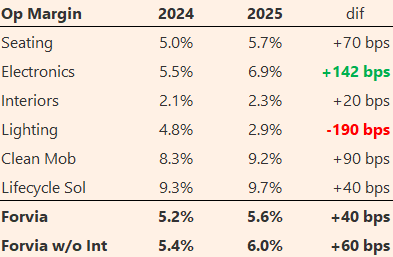

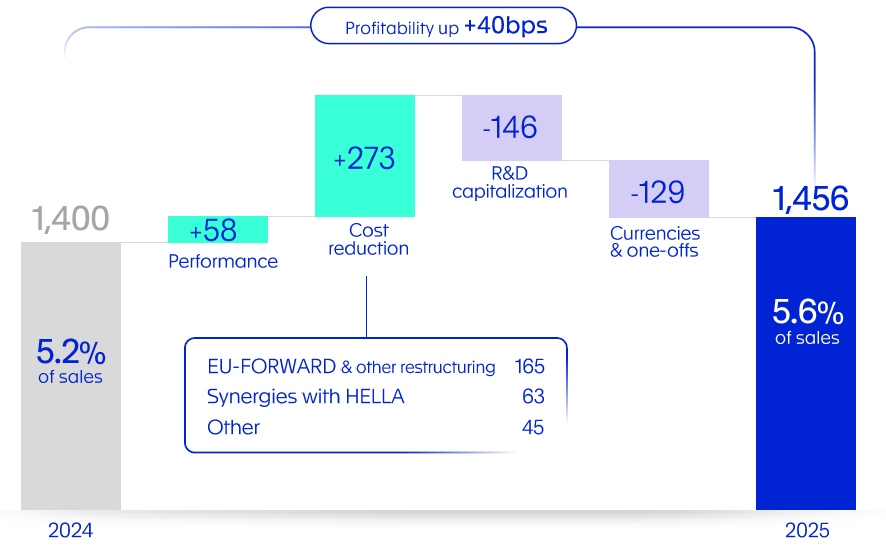

The margin improvement in a flat sales environment has been very positive. Both the EU-FORWARD program and the Hella synergies have outperformed my expectations, with a +20 bps incremental beat over my own estimates.

The thesis goal was to achieve €300 million in savings (compared to the company’s target of €500 million by 2029), and these have practically been reached already in 2025.

Furthermore, if we consider the “new” Forvia (excluding Interiors), the group’s EBIT margin rises to 6%.

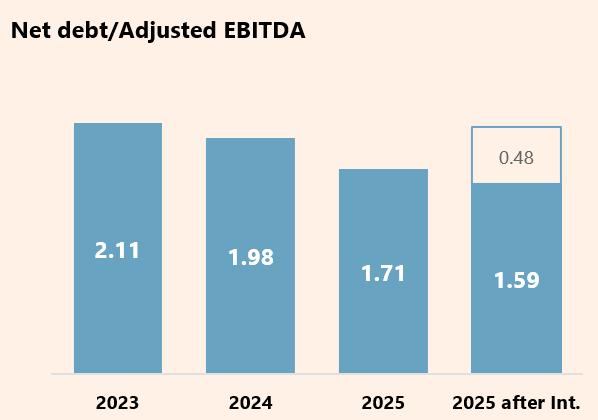

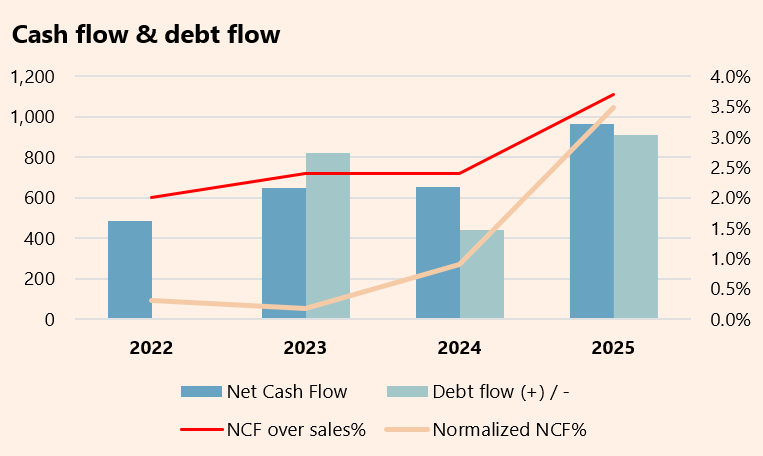

Turning to the debt, there is also good news. In 2025, the leverage ratio dropped to 1.71x, or 1.59x if we factor in the Interiors divestment.

Cash generation has improved despite rising restructuring costs, and the company has reduced its reliance on factoring (client advances with financing costs). This is clearly reflected in the Normalized NCF (Net Cash Flow), which excludes restructuring expenses and the contribution from factoring.

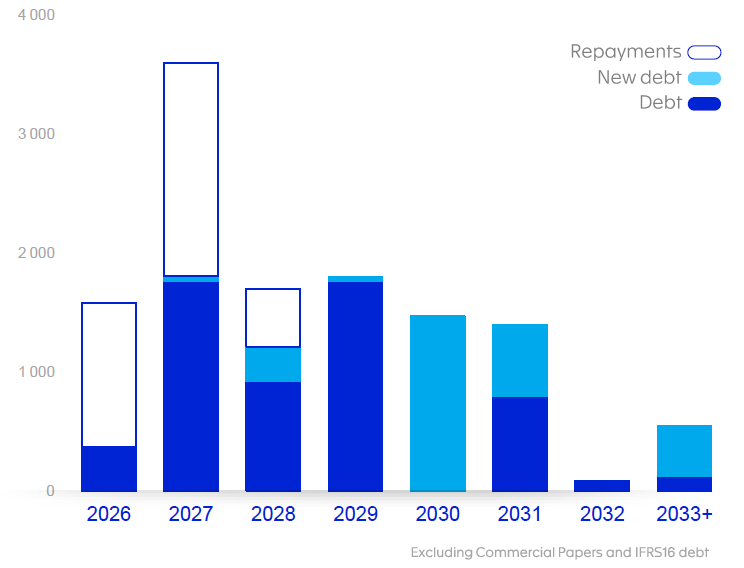

The debt maturity profile has improved, clearing the Everest that 2027 once represented. We hope that this, alongside the stronger cash flow generation and the Interiors divestment, will help improve the company's credit profile, which still sits at the lower end of non-investment grade, with no rating revisions since late 2024.

Let’s take a look at the performance of the main segments.

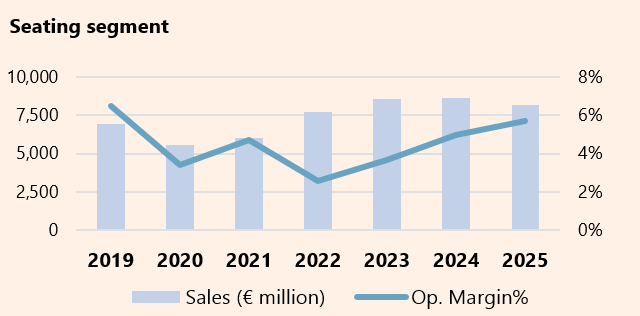

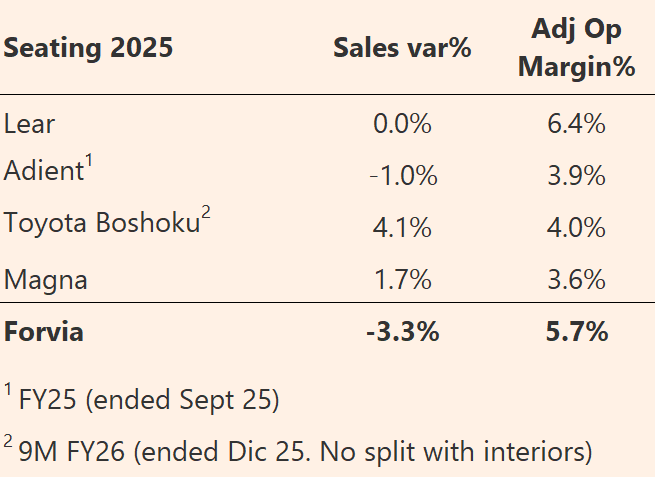

💺 Seating: The Restructuring Paradigm

The Seating segment, responsible for 31% of sales (nearly 40% in the new Forvia), is the textbook example of a restructuring process. The segment’s sales dropped due to the slowdown in the Chinese market—mainly BYD—and the European market, yet margins expanded. The net effect is positive, with a 7% higher EBIT contribution than in 2024.

The underperformance relative to its competitors is primarily explained by its over-representation in Europe, where most of the capacity cuts (under the EU-FORWARD3 program)

The company views the Seating segment (the origin of the former Faurecia) as part of its growth portfolio. This is where management sees the potential for expansion:

Higher CPV (Content Per Vehicle): The shift toward increased comfort leads to a higher cost per seat: heating, advanced reclining features for autonomous vehicles, and even massage functions.

Exposure to the Indian market and Japanese/Korean OEMs.

Growth in the industrial segment: Trucks and machinery.

Let’s not forget that Forvia is the world’s #1 in seat frames and mechanisms, and #3 in complete seats

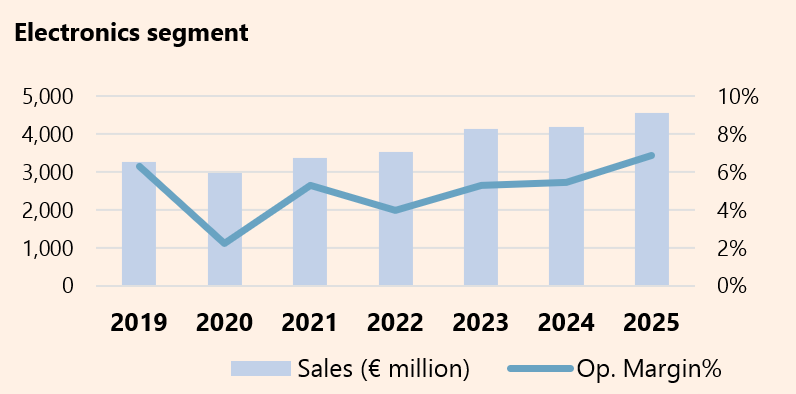

👌👌 Electronics: The Green Shoot

Particularly satisfying is the performance of Electronics, one of the two segments, alongside Seating, that management has classified as “Growth Clusters” in its medium-term strategy. Sales grew by 12% while margins expanded by +140 bps.

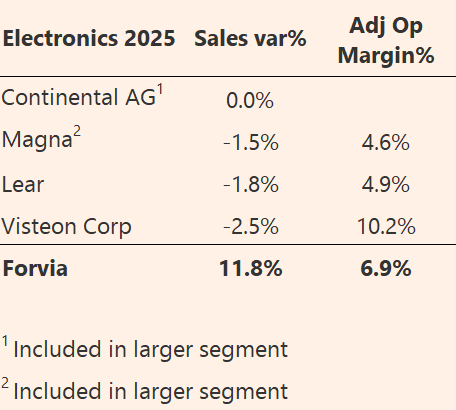

The sales growth relative to its main competitors is highly remarkable.

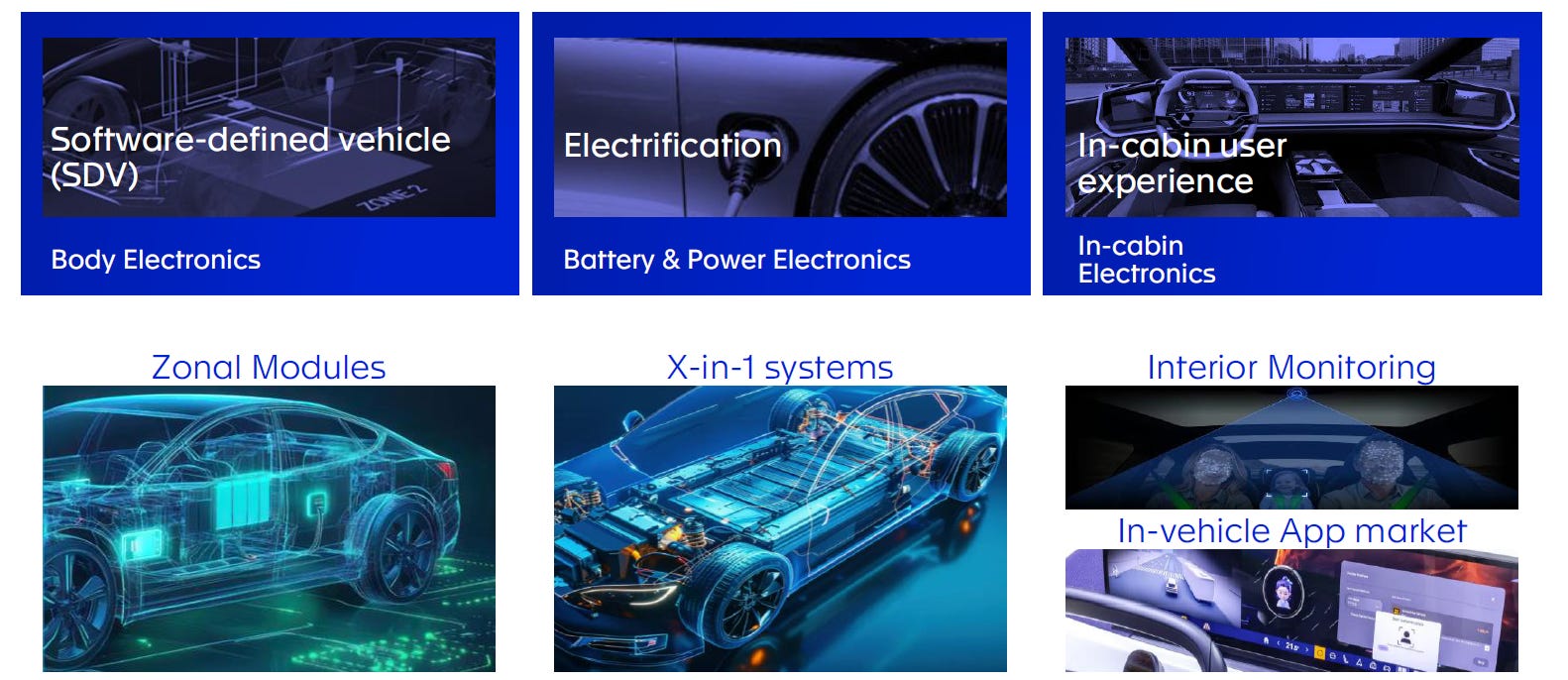

This segment includes radars for autonomous driving and assisted parking systems, power management controllers, and infotainment electronics, among others. It is a segment with very favorable tailwinds, where Forvia is a top 3 global player. Investing in this segment makes perfect sense.

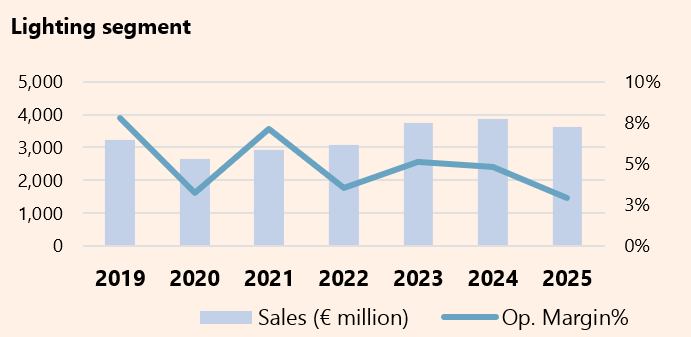

😅 Lighting: The Laggard

The Hella legacy segment is struggling to find its footing. The expiration of several high-volume programs has coincided with a weakening European market. The sector is currently facing clear overcapacity. As a result, the company has recognized a €270 million impairment charge, writing down its goodwill.

This is precisely why Lighting falls into what they’ve labeled the “Value Cluster”: the focus is now on rationalizing investments and reducing capacity to bring the division back to profitability. I believe this strategy is the correct path forward.

🐄 The Cash Cows

The remaining divisions to discuss are Clean Mobility and Lifecycle Solutions. These segments are relatively small (representing 23% of the “new” Forvia’s sales), but their low capital intensity makes them powerful cash generators. There isn’t much to add here: they are improving margins and showing organic growth.

Clean Mobility is the one “sentenced to death”—the division whose terminal value the market essentially prices at zero. I’m not claiming that catalytic converters for internal combustion engines (ICE) are the future, but 71% of new vehicles registered in Europe in 2025 still featured them. The situation in the US is much the same.

“RBC has significantly lowered its 2030 EV adoption forecast for the U.S. from 35% to 17%”

Perhaps this “cash cow” isn't worth zero; perhaps the very weight holding it back will become the catalyst for its value.

🎯 Price Target Revision

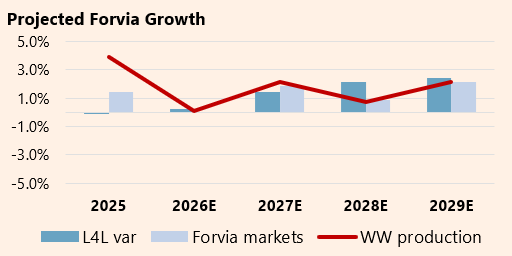

The top-line thesis hasn’t changed much. The industry outlook remains similar: S&P Global Mobility estimates a 1% CAGR (compound annual growth rate) in light vehicle production through 2033. Notable growth is expected in Asia (excluding China) at a 2% CAGR, compared to 0.8% in China. Major Chinese OEMs are currently offshoring their production, and the emergence of India and the ASEAN4 will be key in this process.

Assuming a flat 2026, as guided by management, we are projecting a 1.5% annualized organic growth rate through 2029. This is slightly above the light vehicle production growth in their specific markets (+1.3%).

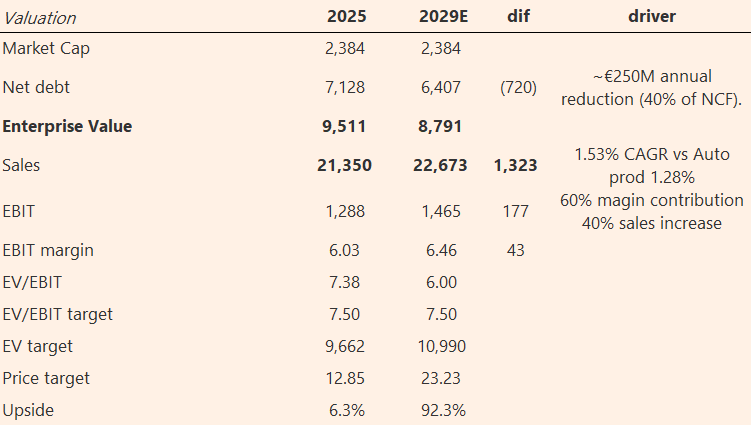

Management has set operating margin targets above 7%, driven by volume improvements and cost cuts. We won’t be quite as optimistic. Forvia’s 2025 EBIT margin, excluding Interiors, stands at 6%.

While I am confident that by 2029 margins will be closer to 7% than 6%, a margin of safety is paramount. Restructuring expenses will remain high, albeit trending lower. By factoring in these projected restructuring costs and a slightly more conservative contribution from the efficiency programs, we are modeling a 6.5% EBIT margin. Debt is projected to decrease progressively, following a conservative path.

This scenario supports a €3 per share increase in our Price Target, representing a 15% bump over our previous estimate. This revision is consistent with our positive assessment of the margin improvements, stronger cash flow generation, debt reduction, and the Interiors divestment.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com

Estimated EV Calculation

Assets held for sale 3.718 millones de €

Liabilities linked to assets held for sale: 2.280 millones de €

Book value of Interiors (excl MateriAct): 1.480 millones de €

This book value accounts for a previously adjusted impairment loss of €553M.

When an OEM prepares to launch a new model or set up production lines, they commission all the necessary equipment. During this phase, tooling sales peak as this equipment is manufactured and delivered. Once production moves into its steady-state phase, these sales drop. Between 2024 and 2025, this effect amounted to €414M, primarily within the Interiors division.

Among other initiatives, Forvia has reduced its workforce by 14% compared to 2024. This division has undergone the largest adjustment, both in net and proportional terms.