Good morning, dear reader.

Today, I want to look back at the first point I wrote in January’s Pond Tracker.

Conviction cannot be transmitted in a thesis, no matter how extensive or well-justified it may be. It is only achieved through two paths (or a necessary mix of both): the authority of the source and, above all, doing the hard work yourself. When I speak of conviction, I mean seeing a 20% drop and using it as an opportunity to buy.

And here we are. With the war ongoing, a large portion of the gains reported in some theses has vanished. The 14% drop in Forvia and the 18% slide in Wizz Air are particularly painful. Let's briefly review each of these investment cases.

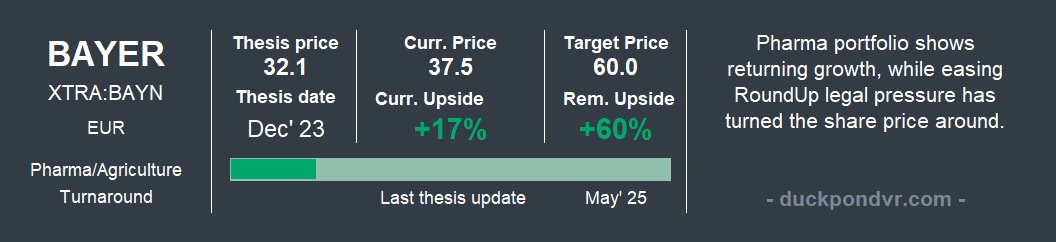

🌱💊Bayer

Bayer has dropped 11% since the start of the conflict. Following the release of its results, the market reacted negatively to the 2026 litigation payout guidance. However, the investment case remains unchanged; I largely reiterate what I stated in the May 2025 update.

In fact, Bayer is attempting to settle the Roundup case for $7.25 billion, which falls within the range I previously estimated ($6.7–$8.4 billion). If they finally close the books on this, the market may once again value Bayer for what it truly is: a solid Pharma player and an agricultural giant.

Immediately following the results, several insiders stepped in to buy. This marks the first time since March of last year that we’ve seen insider purchases, and they are significant amounts.

Bill Anderson, the CEO and architect of the turnaround, purchased 21k shares, bringing his total market position to approximately €8 million. This is nearly double the holding requirement mandated by the board.

udith Hartmann, a member of the Supervisory Board since 2023 and the incoming CFO as of June, purchased 13k shares, an investment of roughly €500k.

Other board members, such as Norbert Winkeljohann and Lori Schechter, also increased their positions by €100k and €70k, respectively.

As the saying goes: An insider has a thousand reasons to sell, but only one to buy.

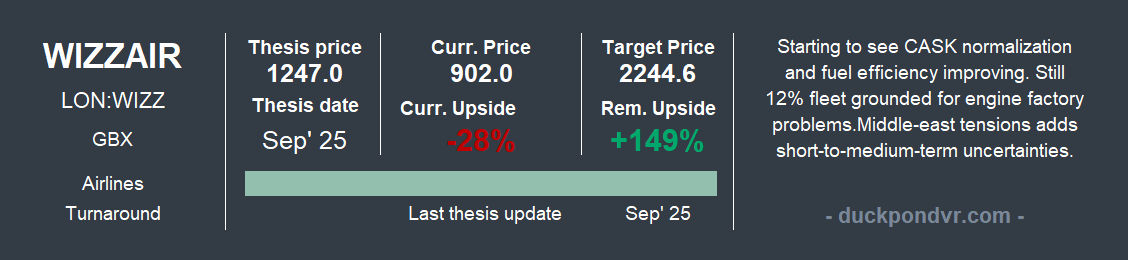

🛫Wizz Air

This is where things get serious: down 18% since the start of the conflict. The impact is direct, hitting through two main channels:

First, approximately 4–5% of sales come from Middle Eastern routes. For now, this will mean a revenue decline. While cyclical, it is certainly not negligible; restoring confidence in international flights to or through the Middle East will take time.

The worst pressure, however, could come from oil: Jet fuel prices surged 58% in just one week, and they tend to be stickier than Brent crude. The war will eventually end. that is transitory, but what will be the lasting echo on global oil supply and, consequently, fuel costs? It’s hard to say.

Amidst this turbulence, the company has already revised its 2026 guidance downward. The 'fuel effect' hits Wizz twice: currency impact (stronger USD) and the rising price per barrel. We’ll dive into Wizz’s hedging strategy another time.

Although I expect the share price could suffer more in the short term, I believe the company has the capacity to reallocate excess capacity to other routes quickly. In the medium term: people flew again after 9/11, they flew again after COVID-19, and they will fly to the Middle East as a destination or hub again.

This is not for the faint of heart, but no one said this would be easy. Despite the clear execution risks, my long-term thesis remains unchanged.

One of the best investments I’ve made to date was IAG (Iberia, British Airways...) in May 2020. As the pandemic progressed, the thesis worsened. It seemed like the end of international tourism. IAG had to launch a rights issue in July; I subscribed 100%. It ended up doubling the investment with an IRR of >40%.

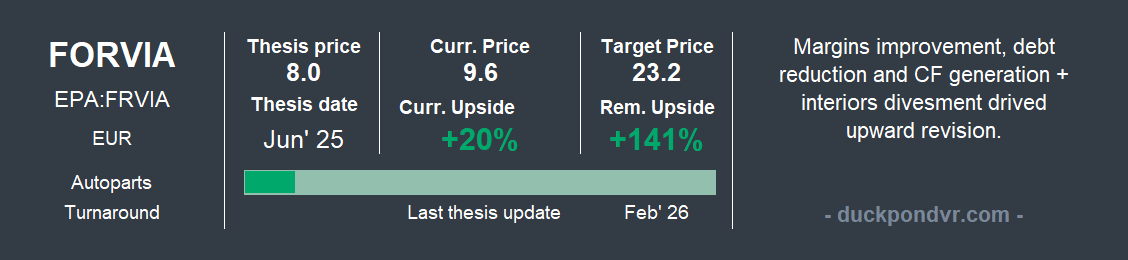

💺⚙️🔦Forvia

The conflict has wiped out 14% of its value since it began. When a confidence crisis hits the markets, everything drops, but the most leveraged companies suffer the most—and that’s exactly where Forvia stands. It is one of the hardest-hit auto parts stocks these days. I see an opportunity here, as I noted in my recent thesis revision.

The 2025 results and the deleveraging outlook appear positive to me. Furthermore, the definitive announcement of the Interiors business sale will loosen the debt noose.

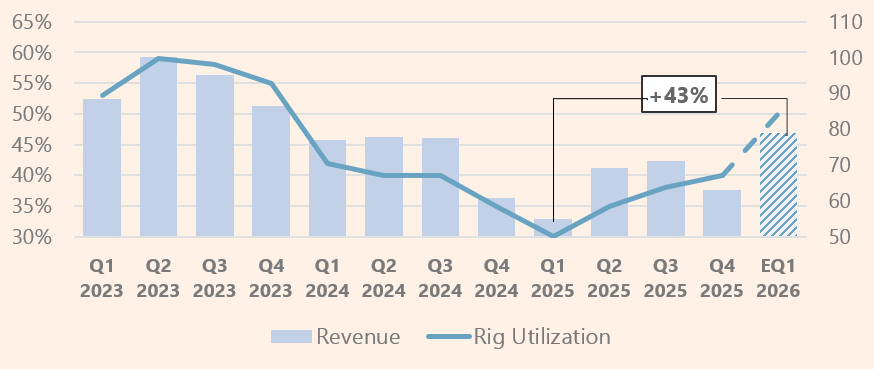

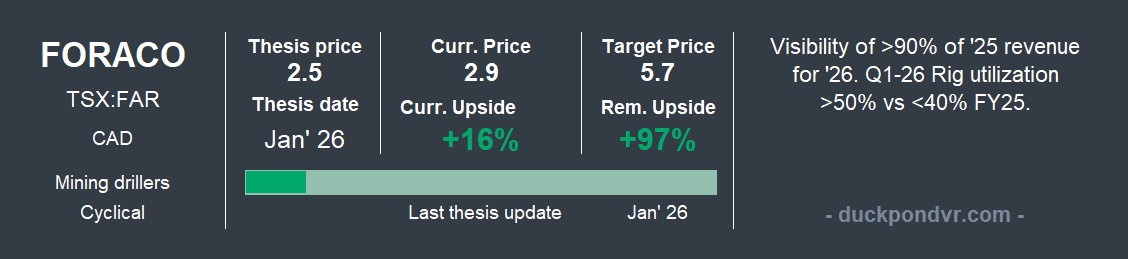

⛏️Foraco

When panic hits the markets and a flight to liquidity ensues, a Canadian listed small cap is the perfect target for investors looking to slash portfolio risk. And that is exactly what we are seeing.

Our favorite mineral drilling company had the worst possible timing for its earnings release: the very Monday the conflict began. It has dropped 12% since then. Has the investment case for gold or copper changed? Has the need for exploration diminished? I don't believe so.

In The Pond Journal #8, I dedicated a section to the 2026 outlook: the order backlog has surged +83% compared to Q4 2024. This backlog provides visibility for 66% of my 2026 revenue estimates and 41% for 2027, with plenty of commercial upside still on the table.

Tim Brenner, CEO of Foraco, confirmed that in Q1 2026, they have already surpassed 50% rig utilization (compared to a 36% average in 2025) and expect to maintain a steady 67% utilization rate. In my projections, maintaining 50% utilization throughout 2026 alone would imply a revenue increase of more than 30%.

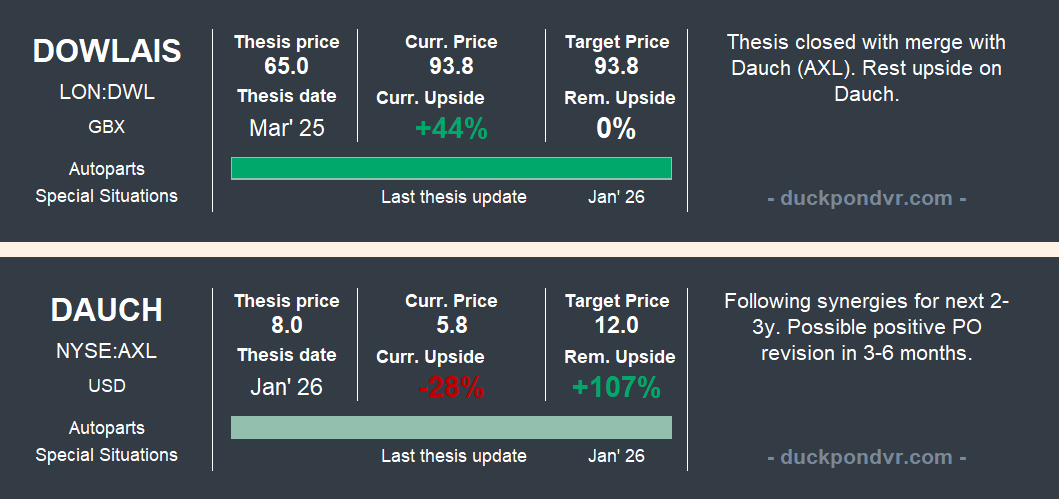

⚒️⚙️🛻Dauch

I saved the most painful case for last: It is true that Dauch hasn’t dropped more than its peers since the start of the conflict (11%), but it was already down 30% since it began trading alongside Dowlais.

One of the primary drivers of this decline has been the market’s skepticism regarding expected synergies and higher than anticipated restructuring costs. There is also an “investor exodus” effect in the UK following the cancellation of Dowlais and the subsequent share distribution. I will analyze this more calmly and provide an update soon.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com