Welcome to The Pond Journal #8. This week, everyone has their eyes fixed on the Middle East, and for good reason. As an investor, you currently have two options: stay informed while trying to manage your emotions, or head out for a walk in the mountains. There is no joy to be found here, except perhaps for those on Polymarket betting on geopolitics with insider information.

Market risk perception is curious, to say the least: Israel’s benchmark TA-125 index surged as much as 6% relative to Friday’s close, while the Eurostoxx dipped over 6%, and the S&P 500 dipped only 1%.

No one knows where these events might lead, but it’s worth remembering that this isn’t the first escalation of tension in the Middle East, and that panics often represent prime investment opportunities.

Last year, the trade war was supposedly set to reshape the world. In April, markets suffered through extreme volatility, and within that chaos, opportunities with highly asymmetric risk-reward profiles emerged.

Two examples:

Semapa: How could tariffs possibly affect a Portuguese holding company whose core business is producing and selling paper, cardboard, and tissue in Europe? The answer is: not at all. Yet, investors fled toward liquidity. On April 7, 2025, Semapa traded 12% below its prior levels, hitting €13.6. Today, it trades at €24 (ex-dividend 2025).

Grifols: While the cross-tariff game could have impacted the company,despite its massive plasma production in the US, their pricing power within a virtual oligopoly served as an authentic shield. It traded 20% down at €7.3; today, it stands at €10.5. Still a bargain, but this is another story.

In times like these, “Cash is King”. This is why Berkshire Hathaway, with Buffett’s successor now at the head, is sitting on a $370 billion cash, roughly 30% of total assets. Waiting for the right moment to strike, like a hunter.

So, what should you hunt? Well, if companies you already know, whose fundamentals are consistently improving, correct due to a massive sell-off, that is your moment

In my last post, I updated the Forvia thesis. The stock, which had approached €15, is now hovering around €10.50. The company’s outlook isn't deteriorating; in fact, I recently revised the price target upward, driven by better margins and higher deleveraging.

Wizz Air could also be an interesting play. Only 4.4% of its active routes are in the Middle East, representing less than 5% of its total revenue. If it was compelling, it still is.

Then there is Foraco. As fate would have it, they presented their results this Monday, a day when commodities and miners were on a true roller coaster. The stock price failed to reflect what was, frankly, excellent news.

I’ll dedicate a section of today’s article to briefly analyzing their results. It doesn't require a full update like Forvia, given that the original thesis is less than two months old.

⛏️A promising 2026

The 2025 results are “bad”, but that was already priced in. The real uncertainty was whether we would see a rebound in Q4, a particularly difficult quarter due to the winter season in Canada and the US. And we did: while the quarter in the North was indeed tough, with revenues dropping 13%, South America surged by 95%. Combined with a 15% growth in EMEA, this offset the decline in North America, leading to a total revenue growth of 4%.

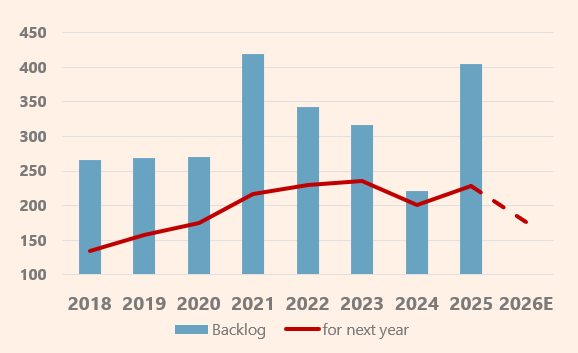

The real silver lining comes from the order backlog, which has skyrocketed by 83% to $404 million. Of that total, $228 million is scheduled for execution in FY2026. While a backlog isn't 'carved in stone,' it provides visibility for 66% of our 2026 revenue and 41% of our 2027 revenue based on our thesis estimates, with plenty of commercial upside still on the table.

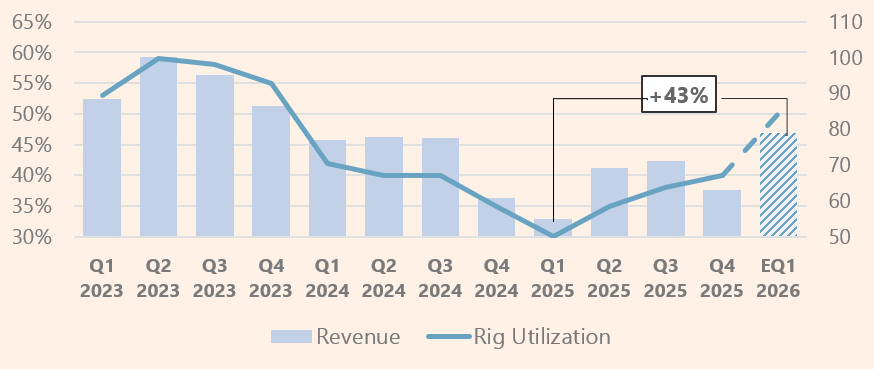

Tim Brenner, CEO of Foraco, confirmed that in Q1 2026, they have already surpassed 50% rig utilization (compared to a 36% average in 2025) and expect to maintain a steady 67% utilization rate. In my projections, maintaining 50% utilization throughout 2026 alone would imply a revenue increase of more than 30%.

“This year, I can tell you that 67% of the fleet is going to be used at any given time” Tim Brenner CEO. Q4 FY25 earnings call.

The company’s record utilization was 74% back in 2012, and management believes reaching those levels again is possible. But step by step, eyes on Q1 2026 now. This rig occupancy could drive a +43% revenue increase over Q1 2025 lows.

Regarding margins, they have weakened, but this is typical given the additional mobilization costs of preparing the fleet for 2026 orders. Debt has also risen slightly, as they have added five new drillers to the fleet over the last six months. The thesis is accelerating, faster than I anticipated. The question remains: will we get a chance to catch it even cheaper?

I’ll see you soon, likely with an analysis of Bayer’s results. Until then, remember that the stock market is a device for transferring wealth from the impatient to the patient.

Thanks for reading the Pond Journal🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com