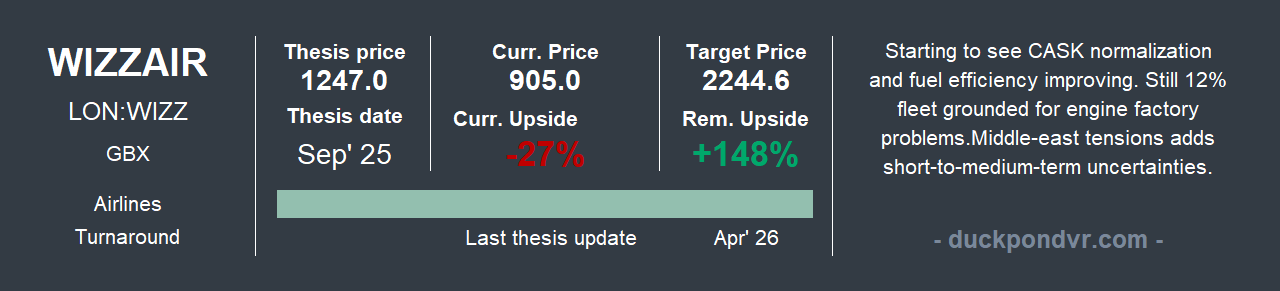

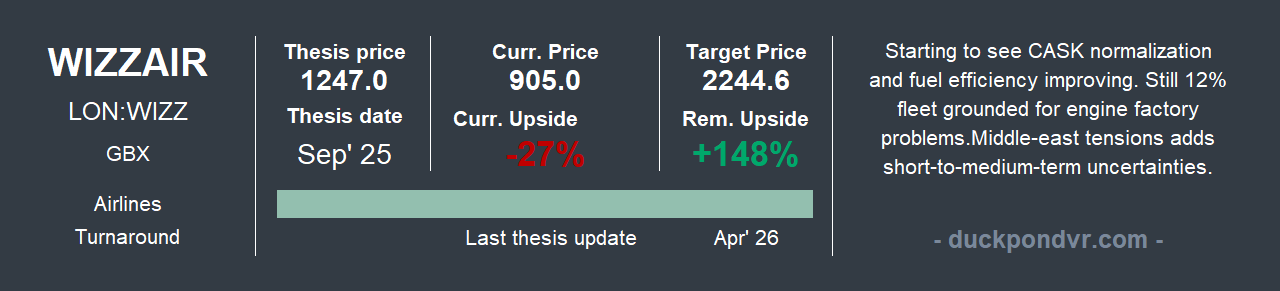

Wizz Air✈️ (LON: WIZZ) — Thesis Update

Short-term shocks are long-term opportunities. Here is why WizzAir still holds despite the drop.

Today we revisit one of the most-read theses in The Value Pond: Wizz Air.

Since the original publication in September, and up until the outbreak of the conflict, the share price remained flat — but today it trades 20% below that level. That alone warrants an update.

The long-term thesis has not changed materially:

Airbus and Boeing continue to face production bottlenecks.

WizzAir’s fleet remains the lowest unit-cost in Europe and is improving in efficiency.

But short-term risks have increased: fuel price and potential shortage, solvency and liquidity concerns, and changes in the shareholder base, all elements worth examining.

In this update we review the fuel crisis, analyse manufacturer bottlenecks, and address one concern about the core thesis. Paid subscribers also get access to the full original dossier and the Excel model.

Content.

Fuel crisis: the Ukraine precedent and cost pass-through

Demand saturation? Q4 FY26 traffic data shows some warning signs

Sale & Leaseback: bottlenecks and debt

Summary

Disclosure and Full dossier + Excel (🔒)

1. Fuel crisis

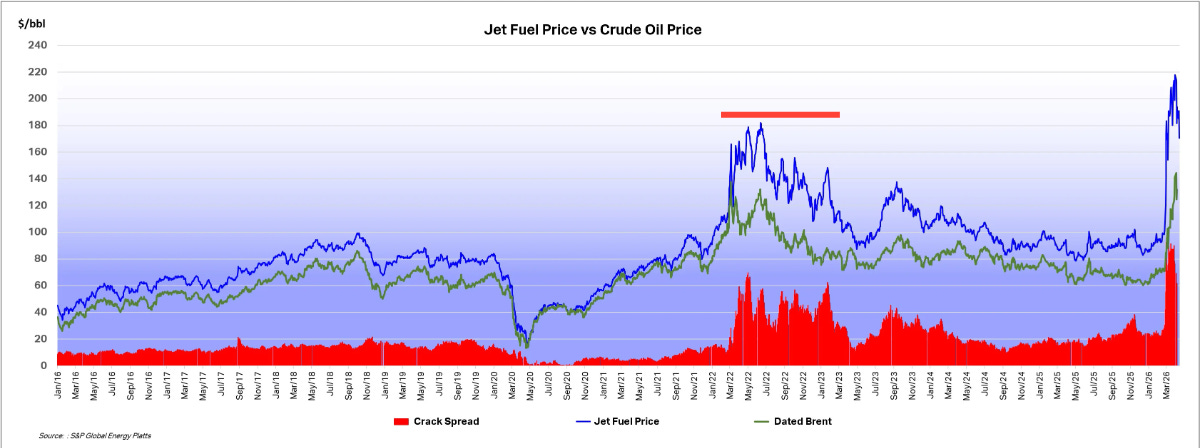

The closest mirror for the current fuel crisis is 2022. When Russia invaded Ukraine, jet fuel prices surged dramatically, reaching $180 per barrel and sustaining an average of $140-150. In the current crisis, prices have reached and held $200 per barrel — potentially the worst energy shock ever recorded.

If there is one lesson from that chart — with the Ukraine war still ongoing — it is what I wrote recently in the Pond Journal #9:

Short term, everyone suffers. Medium term, the economy reroutes.

Despite the war continuing, embargoes, and supply difficulties, jet fuel found its way back to $80-100 per barrel before the current shock. If production capacity in the Gulf is not destroyed and the Strait reopens, the medium-term impact could be even more contained than in 2022, despite being a significant short-term disruption.

This is no longer just a price issue. According to the International Energy Agency (IEA), Europe has approximately six weeks of total reserves before airlines would need to start cancelling flights en masse due to kerosene shortages. WizzAir has already had to resort to full tank loading on some aircraft — increasing weight and therefore fuel consumption — due to supply shortages at certain Italian airports.

We are not going to dwell on the worst-case scenario. And if it materialises, it may create Covid-style opportunities in the sector.

The task of any company facing an uncontrollable external input is to pass costs through to customers. Let us briefly examine how WizzAir handled the previous crisis.

Mission: cost pass-through

After the pandemic, WizzAir eliminated its fuel hedging policy to avoid financial losses from grounded aircraft. In FY2023 that decision proved costly:

Fuel price (average per tonne): $1,218 +54%

EUR/USD: 1.04 -10%

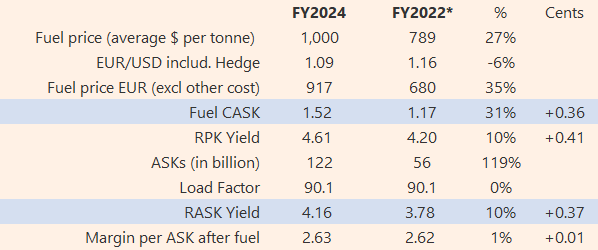

Fuel costs measured as Fuel per ASK rose from 1.17 € cents to 2.00 € cents, an increase of 0.83 cents per ASK, against a Revenue per Passenger Kilometre increase of 0.68 cents per ASK. Results were partially masked by improved load factor (88% vs 78%), though the FY2022 baseline still included part of the pandemic period.

The following year, Fuel per ASK fell 24%, both from lower fuel prices and a partial Euro recovery, declining to 1.52 cents per ASK, while RPK increased 3% to 4.61 cents, recovering the lost ground.

Comparing FY2024 vs FY2022, WizzAir's cost structure did not lose margin due to the fuel increase.

For a fair comparison with FY2022, two adjustments are applied:

FY2024 load factor is applied to FY2022 (still affected by the pandemic)

RPK yield used is from pre-pandemic FY2020, when occupancy was 93.6%.

For context: Ryanair managed to increase its RASK yield by 1.11 cents against a fuel increase of +0.94 cents per ASK, a margin per ASK gain of 0.12 cents. It is worth noting that WizzAir has been growing its ASKs at almost twice the rate.

In WizzAir's favour: the Fuel CASK reflects the competitive advantage of operating a newer, more fuel-efficient fleet with more seats per aircraft. The latest available data (March) shows WizzAir at 50.6 grams CO2 per RPK vs 63g for Ryanair.

FY2027 context

Unlike 2022, the company had learned its lesson this time:

For Q4 FY26 (January-March 2026), over 80% of consumption was hedged at R749/F681 (Roof/Floor).

For FY27, approximately 55% of annual consumption is hedged at R716/F650.

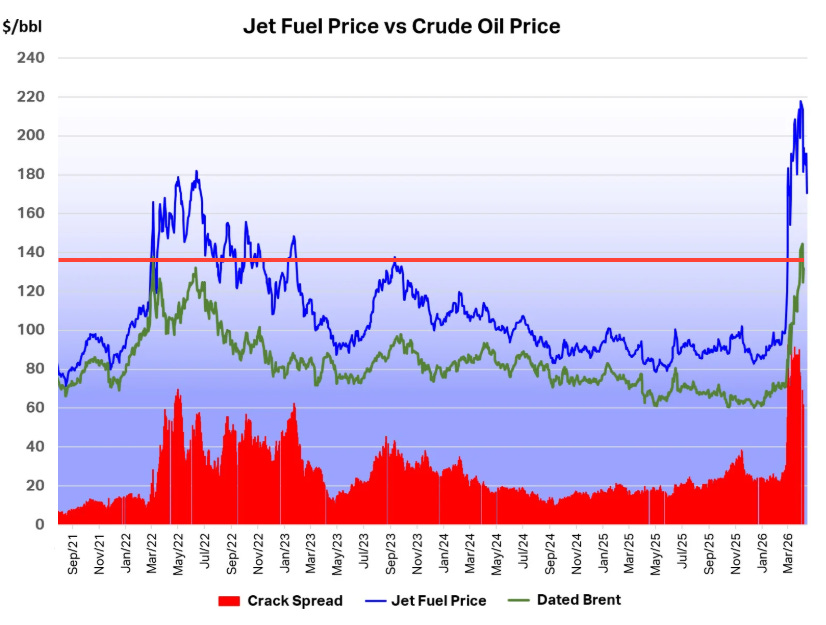

Despite this, fuel CASK in Q4 may have increased to approximately 1.50 cents (from 1.40 in Q3), driven not only by higher fuel prices but also by increased EU Emissions Trading Scheme (EU-ETS) costs.

For FY2027, in a scenario with average fuel at $1,086 per tonne (~$136-137/bbl), reflecting de-escalation and subsequent normalisation, Fuel CASK would increase to approximately 1.59 cents vs 1.43 in FY2026.

WizzAir's Revenue per Passenger Kilometre will close FY2026 at approximately 4.84 cents, with an average aircraft stage length of 1,711 km. This implies an average ticket price (including ancillary) of ~€83. To pass through 100% of the additional fuel cost, that ticket would rise to €86 in FY2027, an increase of 3.6%.

Airlines are already passing costs through to fares, with some applying dynamic fuel surcharges that fluctuate up to the day of departure.

2. Demand saturation?

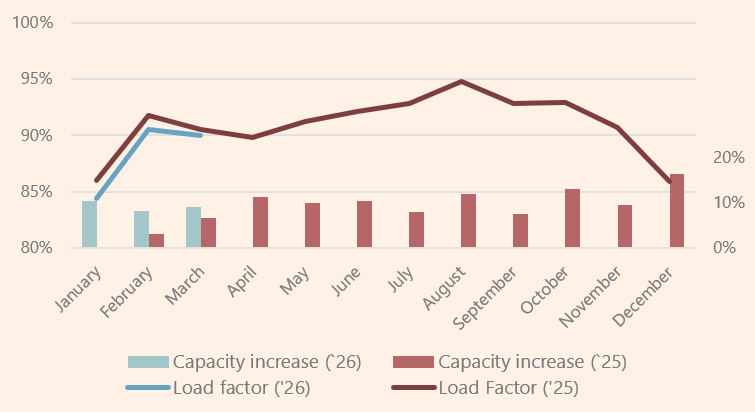

Monthly KPIs show that in FYQ4 2026, load factor was 88.3% vs 89.4% the prior year. With seat capacity up 9.3%, one percentage point less occupancy is reasonable in the weakest quarter of the year with that level of supply growth. So far, so normal.

The concern is the following.

At the end of FYQ3 2026 (calendar Q4 2025), the company had 220 operating aircraft and 209 equivalent operating aircraft (a metric accounting for grounded aircraft and the timing of new deliveries). Entering FYQ4 2026, the weakest demand quarter, with approximately 220+ operating aircraft, and assuming 5 net deliveries (8 in, 3 out) contributing 2.5 equivalent aircraft, we reach approximately 222.5 equivalent aircraft.

The problem: that implies 25% more capacity while seat supply only grew 9.3%. In other words, some aircraft are not flying. The Iran conflict only affects March within FYQ4.

Q4 is admittedly the weakest quarter, but estimated ASKs per equivalent aircraft look low. It is possible the company has sold some of the Airbus aircraft that were due for delivery, which connects directly to the next point and reinforces one of the core thesis arguments: manufacturer bottlenecks.

This is something to monitor in Q1 FY2027 and in the Annual Report when it becomes available.

3. Sale & Leaseback

A brief refresher on WizzAir's growth model:

WizzAir signed a contract with Airbus in 2017 (subsequently updated) committing to a delivery schedule through 2032. Agreed prices are adjusted for Airbus's cost inflation but include significant volume discounts. WizzAir makes advance payments to Airbus during manufacturing (currently approximately €1 billion in prepayments).

When aircraft are delivered, WizzAir can either retain ownership or transfer them to a lessor under an operating lease, the sale & leaseback model. The main advantage: the company recovers all prepayments made to Airbus, funding further growth. The main disadvantage: at lease expiry, the airline does not own the asset.

The company's target is to reduce sale & leaseback to 50% of the fleet, though it currently exceeds 80%. In the current environment, that makes complete sense.

n a normal market, sale prices to lessors tend to equal factory cost plus an availability premium. Aviation is not in a normal market.

Bottlenecks

AerCap's business is buying aircraft to lease, being opportunistic across the cycle. Buy cheap, sell expensive. They do it well: 14% annualised shareholder return over the last 10 years.

What does AerCap's management say about the current situation?

Structural long-term scarcity: CEO Aengus Kelly views delivery delays and supply shortages as a structural problem that will persist at least through the end of this decade and likely well into the 2030s.

Availability premiums: Since airlines cannot rely on manufacturers to deliver on time, immediate availability has become invaluable. Aircraft close to delivery or already available command a significant market premium.

Record sale margins: AerCap sold aircraft from its own portfolio at a 27% gain (equivalent to double book value of equity), a clear reflection of strong demand and the prices buyers are willing to pay.

Returning to WizzAir: as shown in the original thesis, the company was receiving new A321neos at approximately €65 million and delivering them to lessors with an accounting gain of €7-8 million per aircraft. In cash flow terms, the effect is even larger: Upon delivery, the company receives both the gain and all prepayments made during the manufacturing period.

Financial debt

One driver of WizzAir's higher volatility relative to peers is its elevated leverage. On a reported basis, Net Debt / EBITDA stands at just over 4x, high by any measure.

Two clarifications are worth making:

First, financial debt should be reduced by both short-term deposits (essentially cash) and prepayments (~€1 billion). In the sale & leaseback model, those prepayments convert to cash at the moment of aircraft delivery. Adjusting for both, the ratio falls to 2.93x.

Second, when WizzAir receives a new aircraft, two simultaneous positive cash effects occur of very different natures.

The first is the sale & leaseback gain: WizzAir sells the aircraft to the lessor above catalogue price, generating an immediate premium and indirectly funding growth without tying up capital

The second is the capture of the structural negative working capital inherent to the airline model: passengers pay weeks or months before flying, generating a permanent cash float associated with each incremental aircraft added to the fleet. This float is not an accounting profit, it is real cash that WizzAir retains for as long as the aircraft remains operational.

In year one of each new aircraft, WizzAir recovers approximately 20% of the total financed asset value, combining the sale & leaseback gain, the structural negative working capital capture, and operating EBITDA. While bottlenecks persist, the sale & leaseback model makes compelling strategic sense.

4. Summary

Three things stand out from this update:

The fuel shock is real but manageable. WizzAir enters FY2027 with 55% of consumption hedged and a proven track record of passing costs through to fares. A 3.6% ticket price increase covers the modelled fuel increase in full. The precedent from 2022 shows the business can absorb a severe shock without structural margin damage.

The demand signal in Q4 warrants watching. The gap between equivalent aircraft and ASK growth suggests some aircraft are not flying at full utilisation. This is the weakest quarter seasonally, but it is a data point to track in FY2027 Q1 and the upcoming Annual Report.

The sale & leaseback argument has strengthened. AerCap’s commentary confirms that the structural aircraft shortage is not transitory. WizzAir’s locked-in order book at 2017 prices is a genuine competitive advantage, and the cash mechanics of each new delivery remain highly attractive.

The long-term thesis holds. The stock is +20% below September levels and the structural drivers are intact.

5. Full dossier + Excel (🔒)

The full dossier and the Excel model are available for subscribers below the disclaimer.

Full disclosure

WizzAir represents 6% of the total portfolio (Top 4). Several position increases were made during March-April (+2%).

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com