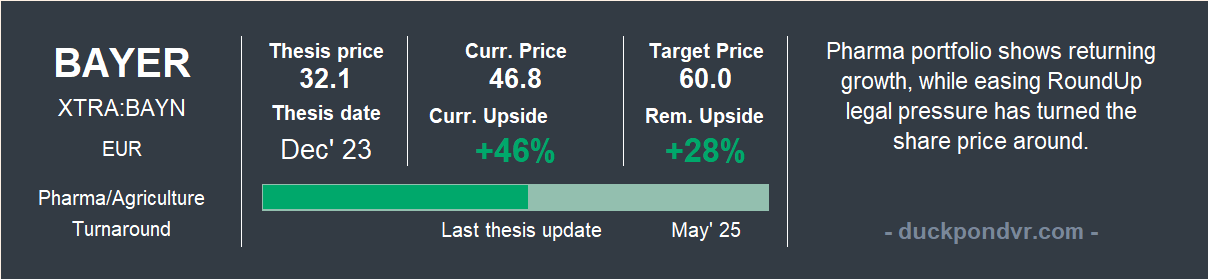

Bayer AG (ETR: BAYN) - Update

Capital prefers a known, pricey ticket over an uncertain meal.

One of the best reasons to run a blog like this when you manage capital on your own, as I do, is that public exposure forces you to question yourself constantly. And that makes you a better investor.

Bayer is probably the most paradigmatic position on the blog in that sense. I wrote a full thesis at a time (Dec 2023) when almost all of Bayer's problems were already on the table. The stock was deeply beaten down. Then it fell further.

I questioned what I had written. More than once I asked myself whether I was wrong. I went back to the thesis, recalculated, re-examined, tightened the scenarios, expanded parts of the analysis… And I kept coming back to the same conclusion: this was going to be a hard road, but there was value here, and it was worth holding.

In the end, you are left with an excellent investment log, which can be summarised in three entries: the full thesis and two major updates.

I have always argued that unlocking Bayer's value depended, and still depends, primarily on putting a number on the total RoundUp litigation bill. Capital prefers a known, pricey ticket to not knowing whether dinner will cost €50 or €500.

Once that is resolved, the conservative valuation rests on the Pharma portfolio holding up. A pharmaceutical company is nothing without patent protection, but patents expire and you need new drugs to replace the ones that run out. Bayer's pipeline was limping, and the expiry of Xarelto combined with the first failure of Asundexian threatened to turn Bayer into a pharma company with declining sales.

The third leg is resolving the discount on a conglomerate of different businesses. Since the Monsanto acquisition, Bayer has never been just a pharma company. Half of revenues come from the Agriculture division, which has significant standalone potential as a leader in a critical global food industry.

The latest developments in the courts shed more light on the first point. Let me explain.

Waiter, the bill, please.

Two events this year need to be read together.

In February 2026, Bayer proposed a settlement of $7.25 billion to close the vast majority of live claims. The stock touched €49 that day.

On June 25th 2026, the US Supreme Court ruled in Bayer's favour on the appeal of the Durnell case, which had resulted in a $1.25 million award in Missouri state courts.

The Durnell case, unlike others with stronger foundations, rested solely on the failure-to-warn claim. By contrast, the more serious rulings against Bayer alleged both design defect in Roundup and negligent conduct by the company.

Beyond the ruling itself, what matters is the doctrine it establishes: the primacy of federal law over state courts. Failure to warn is the foundation that appears in virtually every claim and, more importantly, the one that gave leverage to the mass of modest but numerous cases. By neutralising it, the Supreme Court does not invalidate those cases one by one, but removes their main weapon.

It is precisely this doctrine that will pressure plaintiffs to accept the settlement proposed in February. This does not mean the serious cases disappear: those based on design defect and negligence can still proceed and be litigated individually. The €7.25 billion figure won't surprise long-time readers, I tried to size this exact invoice and landed on roughly $7 billion of remaining payments.

Back to the restaurant analogy: the price of the set menu is almost locked in. We still do not know what the champagne is going to cost.

The ocean liner is turning

In the original thesis, my SOTP always assumed a Pharma division that held steady. Not growing. R&D is not a motorbike. It is an ocean liner. Getting it moving again takes time.

Bayer presents H1 2026 results on 4th August, which will allow me to extend the analysis further. For now, let me briefly cover where the Pharma division stands, that necessary pillar for unlocking the value.

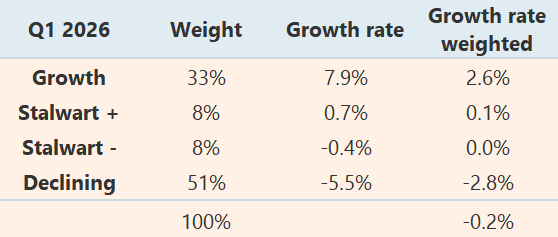

In trailing terms, and applying the methodology I have used before (see Pharma portfolio - Original thesis), the portfolio remains flat. But there are reasons to believe the inflection point is approaching.

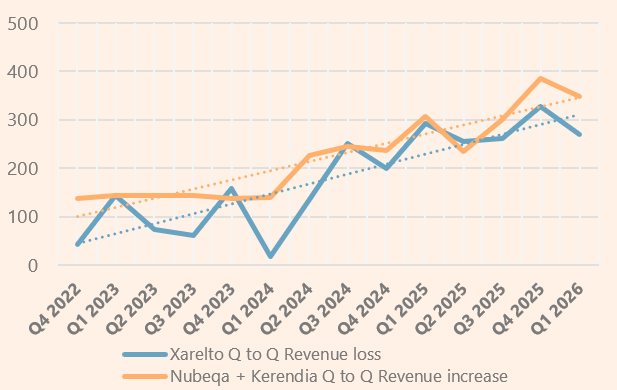

Over 2025 and into 2026, Bayer landed three new drug approvals, added two new uses for existing winners, and posted six positive late-stage trial readings. Nubeqa and Kerendia, the two young drugs I leaned on in the original thesis, are still climbing and offsetting Xarelto’s revenue loss.

New names have joined the line-up too: a menopause treatment, a heart-condition drug, and a targeted lung-cancer therapy, each opening a fresh market. None of this shows up cleanly in a trailing snapshot yet, which is exactly why the division still looks flat.

The second half of the year is expected to deliver stronger top-line growth than H1. However, margins are anticipated to face pressure in the coming quarters due to increasing growth investments behind product launches and the R&D pipeline.

The Agriculture division and the potential spin-off of businesses will be covered in a future update.

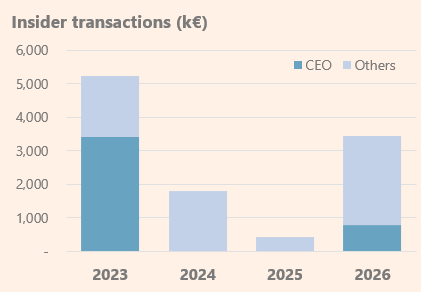

Skin in the game, at last

After three years of drought, where in 2023 most insider purchases were those contractually required from incoming CEO Bill Anderson, in 2026 so far, seven insiders have bought €3 million worth of shares in the open market.

As they say: a thousand reasons to sell, only one to buy.

Latest on the Value Pond

🔒 Associated British Foods (LON: ABF) — Full thesis. Primark alone may be worth the entire group's market cap, with the announced spin-off as the catalyst. Grocery, Ingredients, Sugar and Agriculture come effectively free.

🔓 Semapa (LSI: SEM) — Net cash, listed assets, a 49% discount to NAV, and a controlling family that already tried to take it private once. The signals point to a second attempt.

🔓 The Pond Tracker | Apr '26 — Portfolio review & Q1 snapshots across all active theses.

🔒 Dunelm (LON: DNLM) — Full thesis on the UK's homeware leader. Exceptional quality, 8-10% dividend yield, and one question that determines everything: can it replicate its superstore model in urban centres?

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com