Good morning, dear reader,

We close a disastrous April, where the portfolio's correlation to oil has been strongly negative 😂. Buying Brent puts would have been the most efficient hedge.

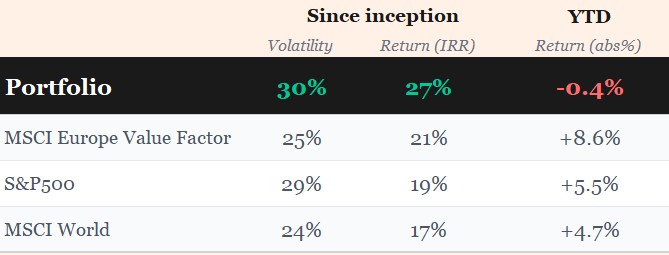

That said, it is worth putting things in context: the annualised return stands at 27% despite a negative YTD.

Investing is, most of the time, about facing discomfort. Right now it is tremendously uncomfortable to hold positions in European car manufacturers, airlines (just as it was during Covid), or SaaS companies, for example. But the truth is that most positions that generate good returns are, or have been, very uncomfortable to hold at some point.

And uncomfortable as it may be, this is no less the right moment to review the open theses on the blog. Let's go.

Reminder: the annual subscription discount ($400/year) is open until May 31st. Check your Mail Inbox (suscribers).

Active ideas

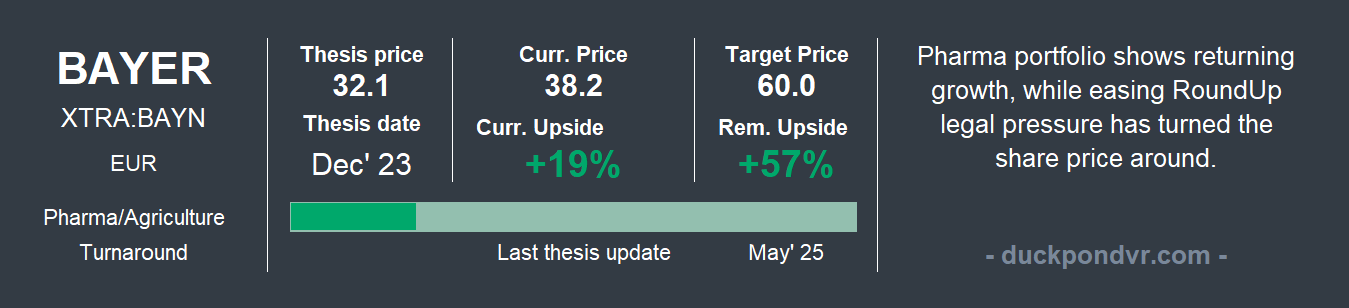

🌱💊Bayer

Bayer has dropped ~6% since the outbreak of the conflict. Here, volatility has been amplified by the start of proceedings at the US Supreme Court on the RoundUp cases.

The next few months are decisive. The Supreme Court's ruling, expected by June, will determine if Bayer can finally cap its liabilities. I expect so.

Q1 2026 results are due on May 12th. We will be watching the pharma portfolio and cash generation closely. Also insider purchases, which were quite active in early March. We will talk more about Bayer then.

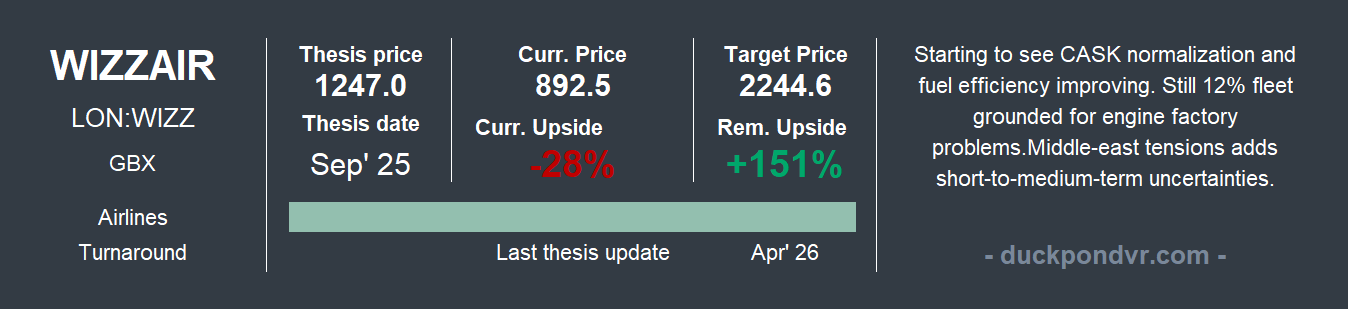

🛫Wizz Air

Wizz Air is down 26% since the outbreak of the conflict. Here, the discomfort maxim mentioned above will be applied rigorously: there may still be further downside.

Today, the idea of flights being cancelled due to fuel shortages no longer seems far-fetched. The peak season for European tourism is now beginning (Q2 and Q3), and this would be a significant blow to the sector. Once again, this is cyclical, not structural. I published an update to the original thesis covering the main risks of this scenario:

Recently, aviation analytics firm Cirium, in its Annual Review 2025, ranked Wizz Air #2 globally in passenger CO2/ASK efficiency for 2025 at 52.9g, despite the grounded fleet. It also operates the #2 youngest fleet globally.

The lower fuel consumption, added to the higher seat density of the A321neo makes structural unit cost advantages and margin resilience.

This is not a recommendation, but I have explained to paid subscribers why I decided to increase my position

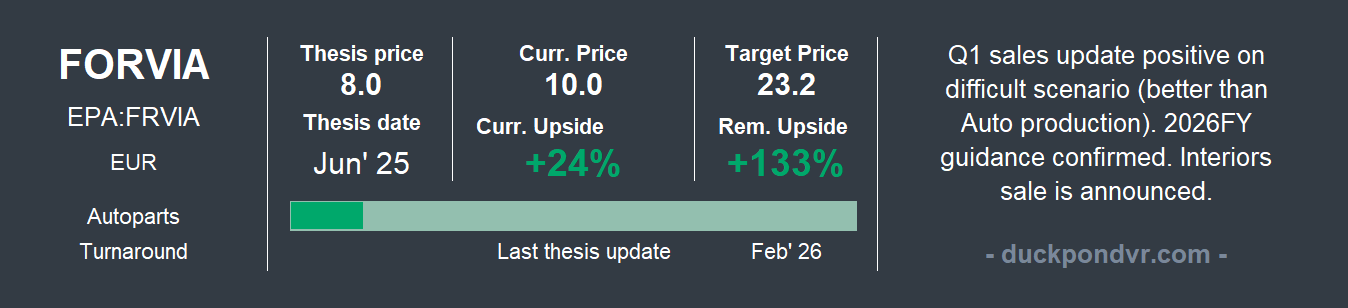

💺⚙️🔦Forvia

Equally uncomfortable, but for different reasons, Forvia has fallen 19% since the outbreak of the conflict. Here, the risk the market sees is that already fragile vehicle demand could deteriorate further if oil prices drive inflation and, in turn, rate hikes and recession.

For its part, Forvia delivered a more than reasonable Q1 given the circumstances, alongside the definitive announcement of the sale of its Interiors division to French private equity firm Apollo for €1.8 billion. This will help reduce leverage risk and smooth volatility.

Q1 FY26 Results Snapshot

Sales €5,135m (-2.2% org, -6.4% rep), +120 bps vs. market.

Drivers: Heavy FX impact. Org. growth in all regions except big drop in China (drop in BYD production impacting Seating).

Outlook: FY26 guidance confirmed (Sales €20-21 billion, 6-6.5% op. margins)

I see no reason to change what I said in the last update, which I leave here:

Worth noting: Spanish value manager Horos has opened a position in Forvia bonds through its fixed income fund. Given the reputation and respect I have for their managers, this is a positive signal.

If you enjoy reading fund manager letters, you should not miss Javier Ruiz, their CIO, in his Q1 letter.

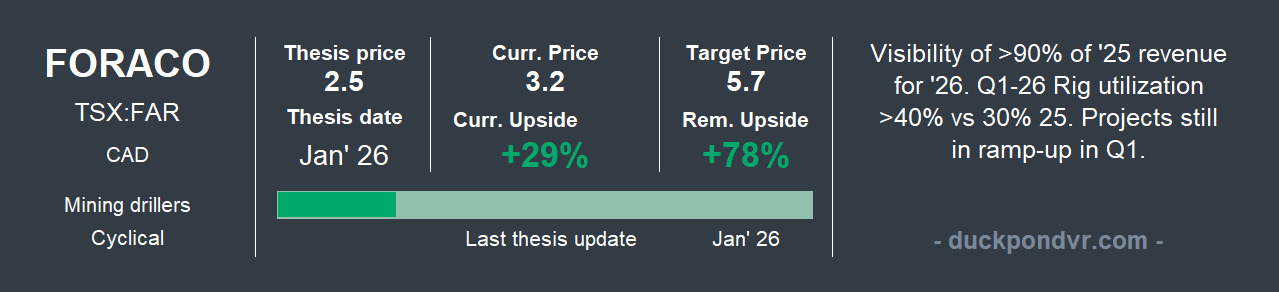

⛏️Foraco

Despite Q1 results already showing early signs of what is beginning in the metals drilling cycle, Foraco is down 5%. In the short term, Foraco is reacting directly to gold and copper prices. Whether gold is at $4,000 or $5,000 per ounce, the need for drilling is not going to stop.

Q1 FY26 Results Snapshot

Sales $66.3 (+20.4%), GM 10.7% (-340bps), EBIT margin 3.1% (-220bps), Net Profit $0.1m. Net debt $90.9m. KPIs: Rig utilization 40% (vs 30%)

Drivers: Solid Mining (+30%), NA (+39%) & SA (+98%). Soft Water (-18%) & APAC (-31%) due to contract phasing. Lower-margin cause og ramp-up phases of new long-term contracts.

Outlook: Highly favorable, underpinned by a record $404 m backlog secured at year-end.

This is one of the best picks I have right now. Not only for the upside, but for the catalysts. The cycle momentum, the size and the operating leverage make it one of the best-positioned names for 2026-27.

⚒️⚙️🛻Dauch

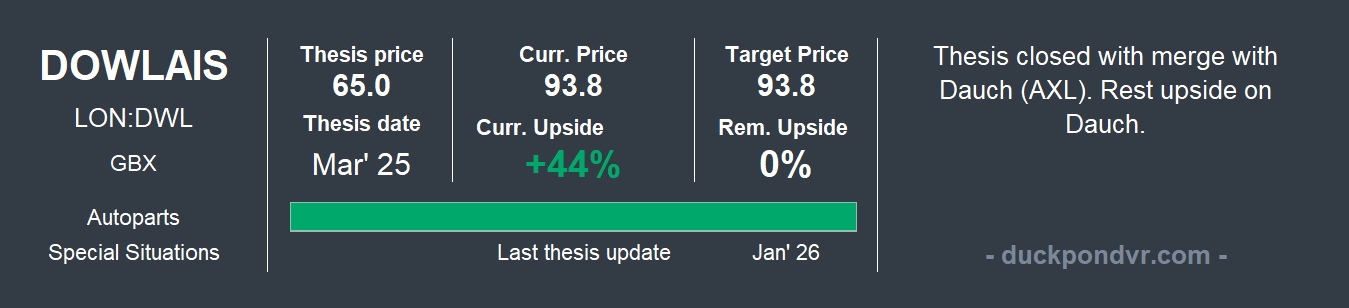

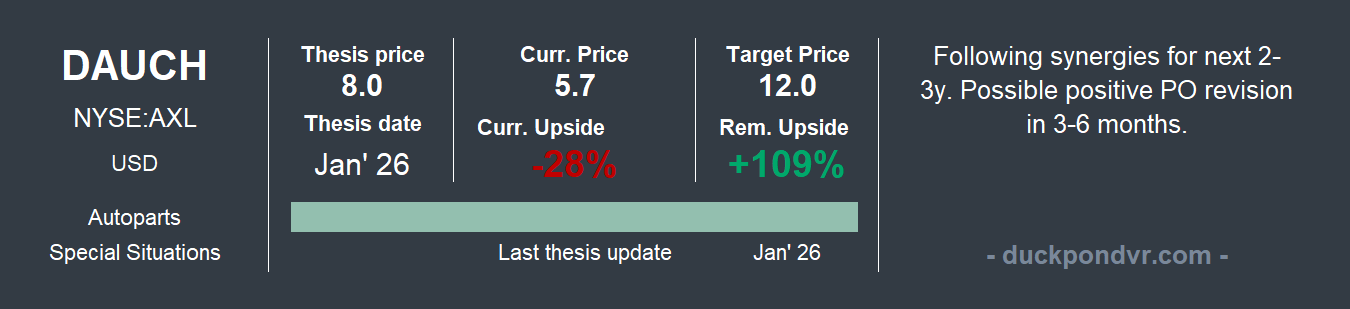

Dauch is down 13% since the outbreak of the conflict, for reasons similar to Forvia, although its lower exposure to Europe helps. One of the primary drivers of this decline has been the market's skepticism regarding expected synergies and higher than anticipated restructuring costs. There is also an investor exodus effect in the UK following the cancellation of Dowlais and the subsequent share distribution. I will analyse this more calmly and provide an update soon.

‘Wait & see’ ideas

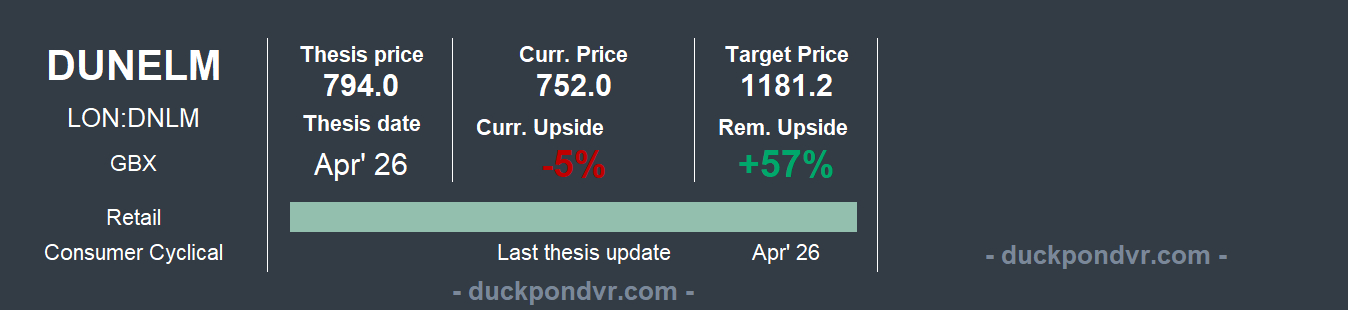

🛏️🛋️🍽️Dunelm

The British homeware retailer is down 25% since the outbreak of the conflict, 33% YTD. This situation is precisely what drew me to this company, which is undoubtedly high quality and has demonstrated consistency in its growth and margins through difficult periods.

That said, the slowdown in Q2 and its confirmation in Q3 did not convince the market, as Dunelm trades on demanding multiples.

Q3 FY26 Results Snapshot

Sales £472m (+2.1%), YTD Sales £1,398m (+3.1%), GM +30bps, Digital 43% (+2ppts)

Drivers: Uncertain consumer environment, customer shift towards discounted products over full price ,Middle East instability (minor direct impact expected).

Outlook: No immediate consumer confidence improvement assumed. FY26 PBT guided to lower end of consensus (£210m-£217m). Accelerating store openings next FY (Kingston-upon-Thames in summer)

As I said, the company has many positive attributes but lacks the margin of safety I look for. You can draw your own conclusions by reading the full thesis. It may offer a good opportunity in the coming months.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com