Good morning, dear reader,

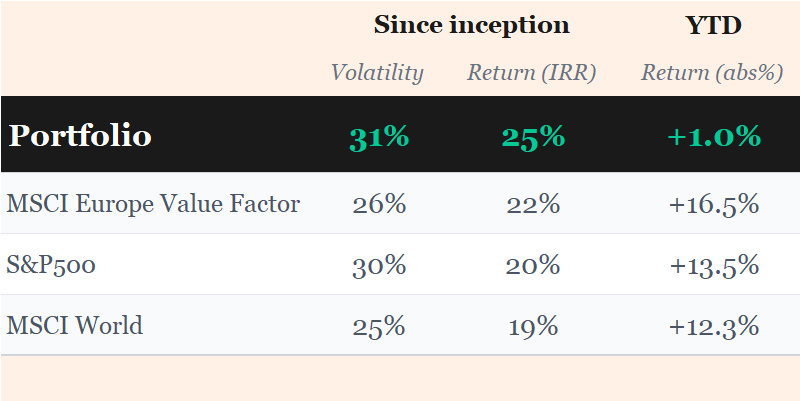

We closed a plain H1 in the portfolio, and looking back, that might actually be a win. We navigated a very volatile H1, with autoparts, which had been driving 2025's returns, heavily punished in the portfolio.

Even though the war was the trigger for the drawdown, and other sectors have been recovering since, autoparts haven't, getting dragged into a pessimistic cycle narrative alongside their OEM customers. Gold and gold miners, despite carrying less weight now, have also given back their gains.

All this in a context where double or triple digit YTD returns are proliferating in semiconductor or memory stocks. But that's not my game, I feel I have no edge there, and I'd basically be speculating. I have nothing against that, but when we're talking about six figure positions or seven figure portfolio with money that isn't yours, what lets me sleep at night is knowing exactly what game I'm playing.

That said, it’s worth putting things in context: the annualised return stands at 25%, with positive YTD after a good May and a not that bad June. Clients are satisfied, and the year starts fresh.

Let’s go through the main open theses at The Value Pond.

Active ideas

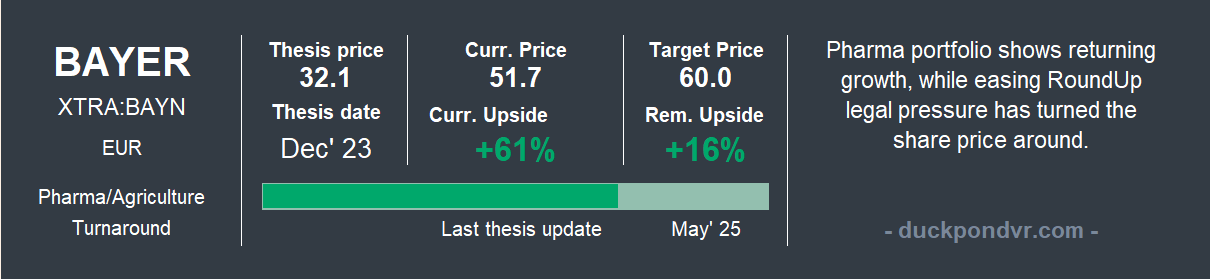

🌱💊Bayer AG

Since the last Pond Tracker, Bayer's share price is up 40%. The June 25th Supreme Court ruling on the Durnell case was the key driver. I discussed it in this recent post.

With the litigation menu closer than ever to a final number, attention is shifting to the Pharma portfolio and to unlocking the company's value, maybe through a Consumer Health sale? An Agriculture spinoff? We'll see.

For now, we reaffirm the target price, already very close to €60, though I wouldn't rule out updating the original thesis to revalue a Pharma portfolio that's no longer limping as badly, or an Agriculture division with real potential in an agricultural cycle caught in a standoff between trade blocs.

Next results: H1 2026 on August 4th.

P.S: Word out there is that DCA-ing into a falling stock is a terrible investment method. I started with Bayer in September '23, added in April '24, and topped up again in August '25. With an average purchase price under €34, the IRR is already above 20%.

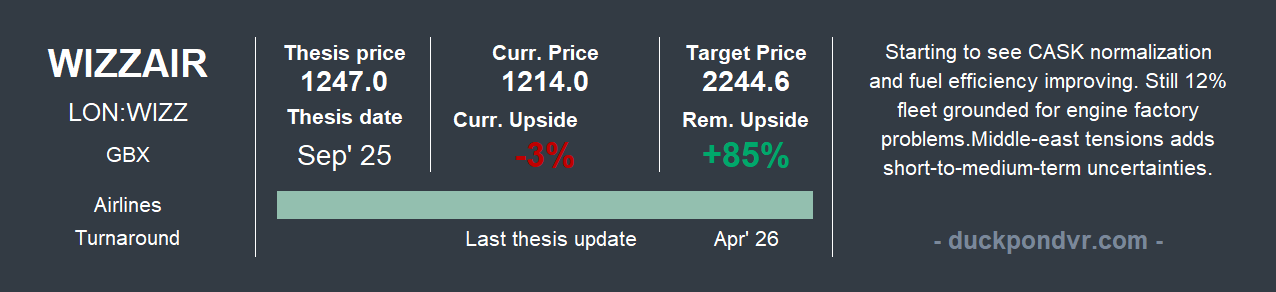

🛫Wizz Air

Back in April, facing the risks from rising fuel prices, I gave Wizz Air the update it needed. To me, the risk was contained and limited in time. It played out exactly that way.

The stock is up more than 30% since the last update, and one of the risks that moderately worried me in April, whether demand could absorb such a large increase in capacity, has been easing.

We'll see at what ticket prices, but demand is consistently absorbing capacity increases of over 20% in the most demanding year of the fleet delivery schedule through 2030.

On top of that, the FY2026 Annual (Apr'25-Mar'26) slightly narrowed expected losses, which drove a favourable reaction.

Next date: Q1 FY27 (Apr-Jun) on August 6th, where I expect to see the ticket price trend heading into the most important quarter of the year, Q2. I'll keep posting the monthly traffic chart on X (link).

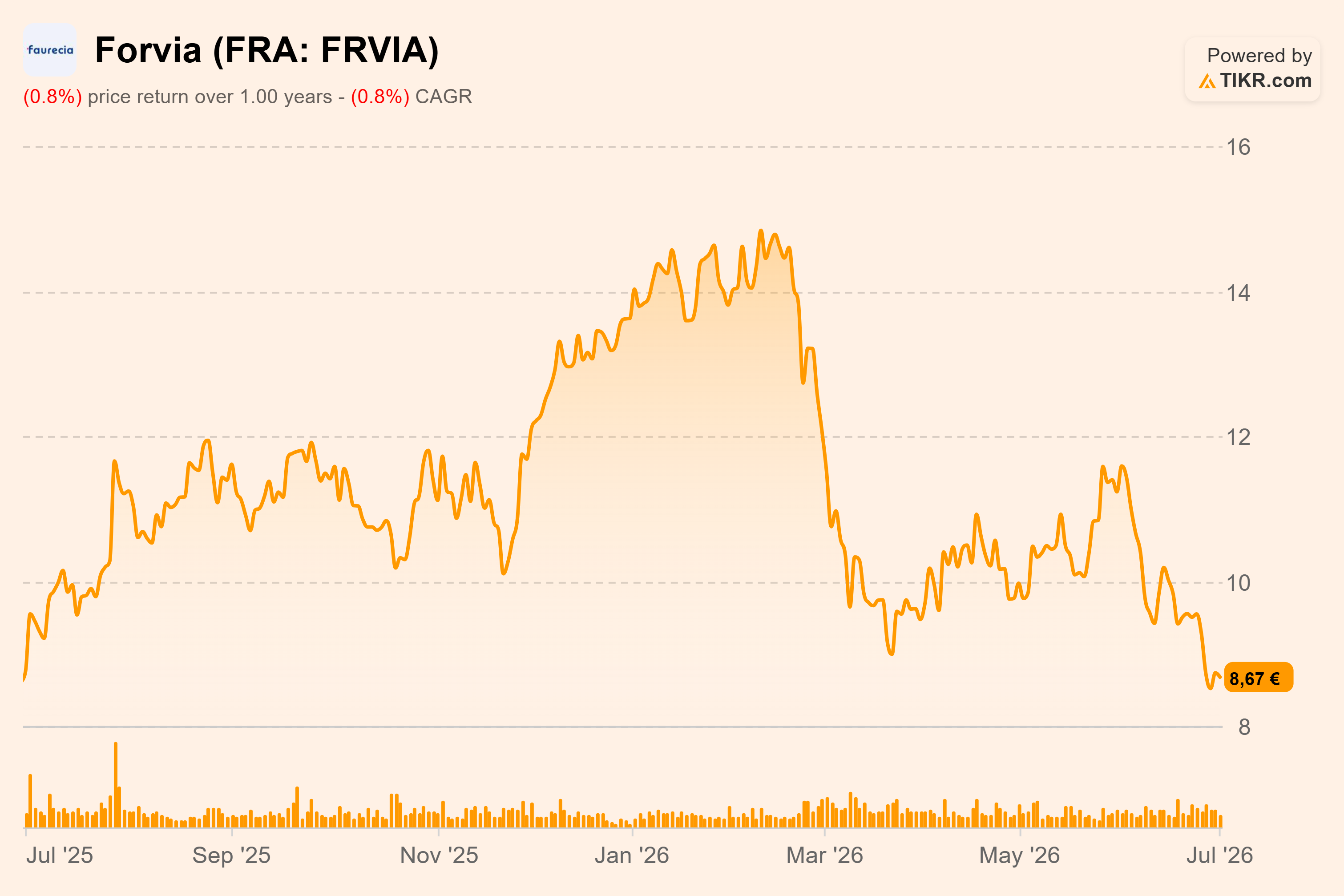

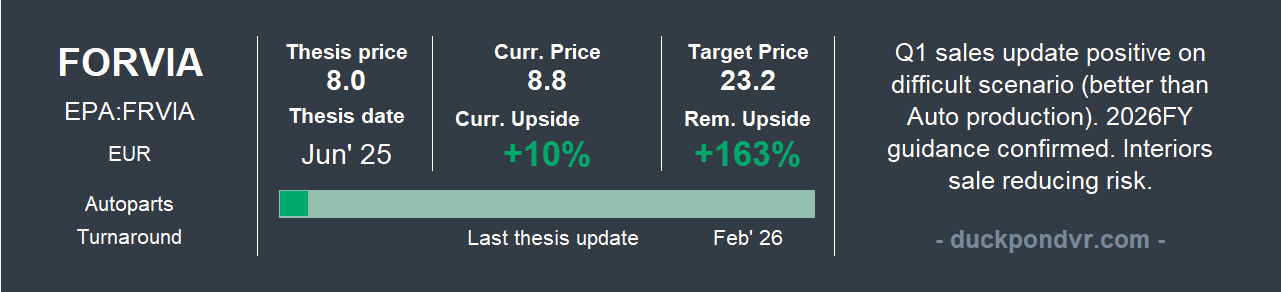

💺⚙️🔦Forvia

As I've said before, the war was the trigger for the drawdown, and while other sectors have recovered, autoparts haven't kept up. The sector has bought into a pessimistic narrative alongside its OEM customers. The market is punishing Forvia due to Volkswagen's restructuring, a path that Forvia itself has already been carving out over the last two years. Volkswagen's layoff announcement reinforces that negative narrative around European vehicle demand (17% of Forvia's sales). I think the market's reaction is understandable, even if it hits indiscriminately, but weren't we already pricing in pessimism on auto production?

It's a shame, because on a fundamental level Forvia had been delivering on expectations, propelling the stock above €14 in February on the announcement of the Interiors sale.

All of this remains buried under sector pessimism, so I see no reason to change what I said in the last update, which I leave here:

I’m not adding at these prices, because I decided to cap total portfolio exposure. You shouldn’t overexpose yourself to such a cyclical sector when the bottom of the cycle isn’t clear yet.

On July 31st, they report H1 results, where we’ll see if they confirm performance slightly ahead of auto production. After the narrative driven sector wide hits, results are what separates the wheat from the chaff.

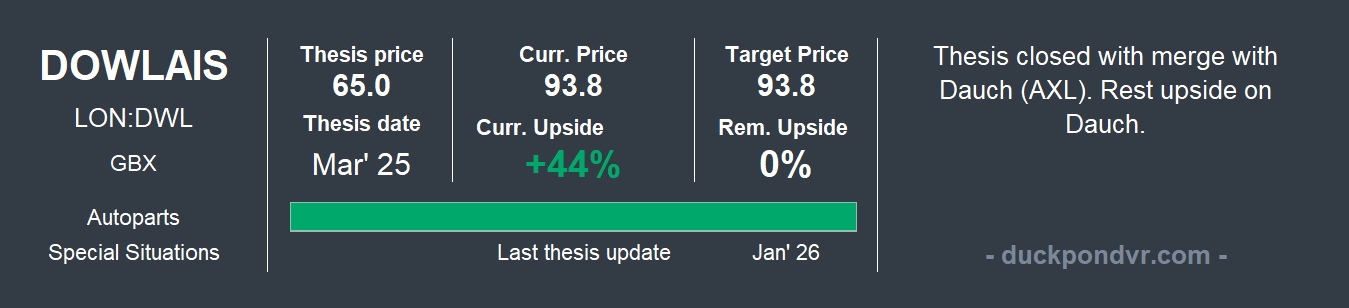

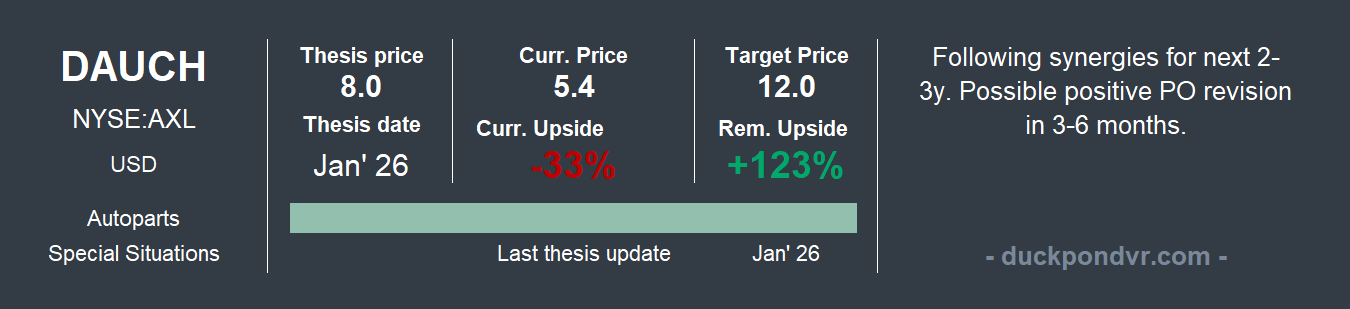

⚒️⚙️🛻Dauch

Dauch is down 13% since the outbreak of the conflict, for reasons similar to Forvia, though its lower exposure to Asia/Europe has softened the blow somewhat. One of the primary drivers of this decline has been the market's skepticism regarding expected synergies and higher than anticipated restructuring costs. There is also an investor exodus effect in the UK following the cancellation of Dowlais and the subsequent share distribution. I will analyse this more calmly and provide an update soon.

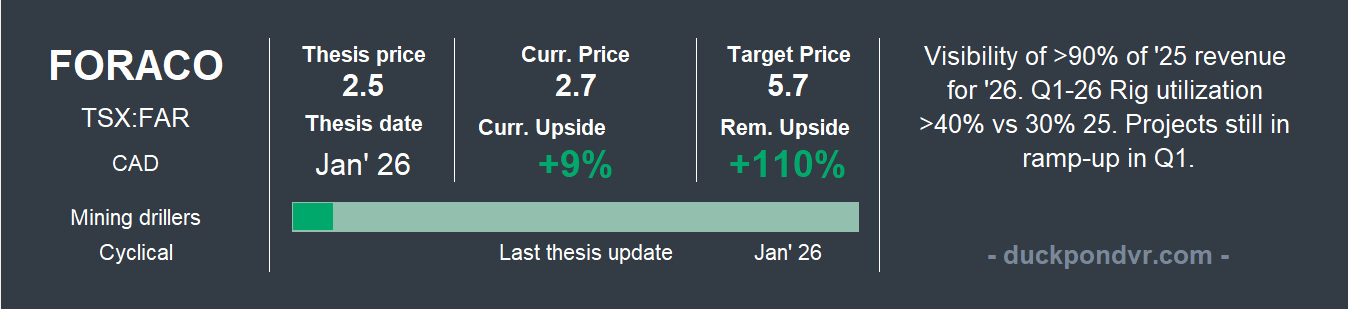

⛏️Foraco

Foraco is going through natural back and forth, typical of a stock with such thin market volume. In the last tracker it was at 3.2 CAD, and it's now trading around 2.8 CAD.

Foraco's short term moves depend mostly on gold's moves. But Foraco's business, or gold miners' business in general, isn't built on short term commodity volatility.

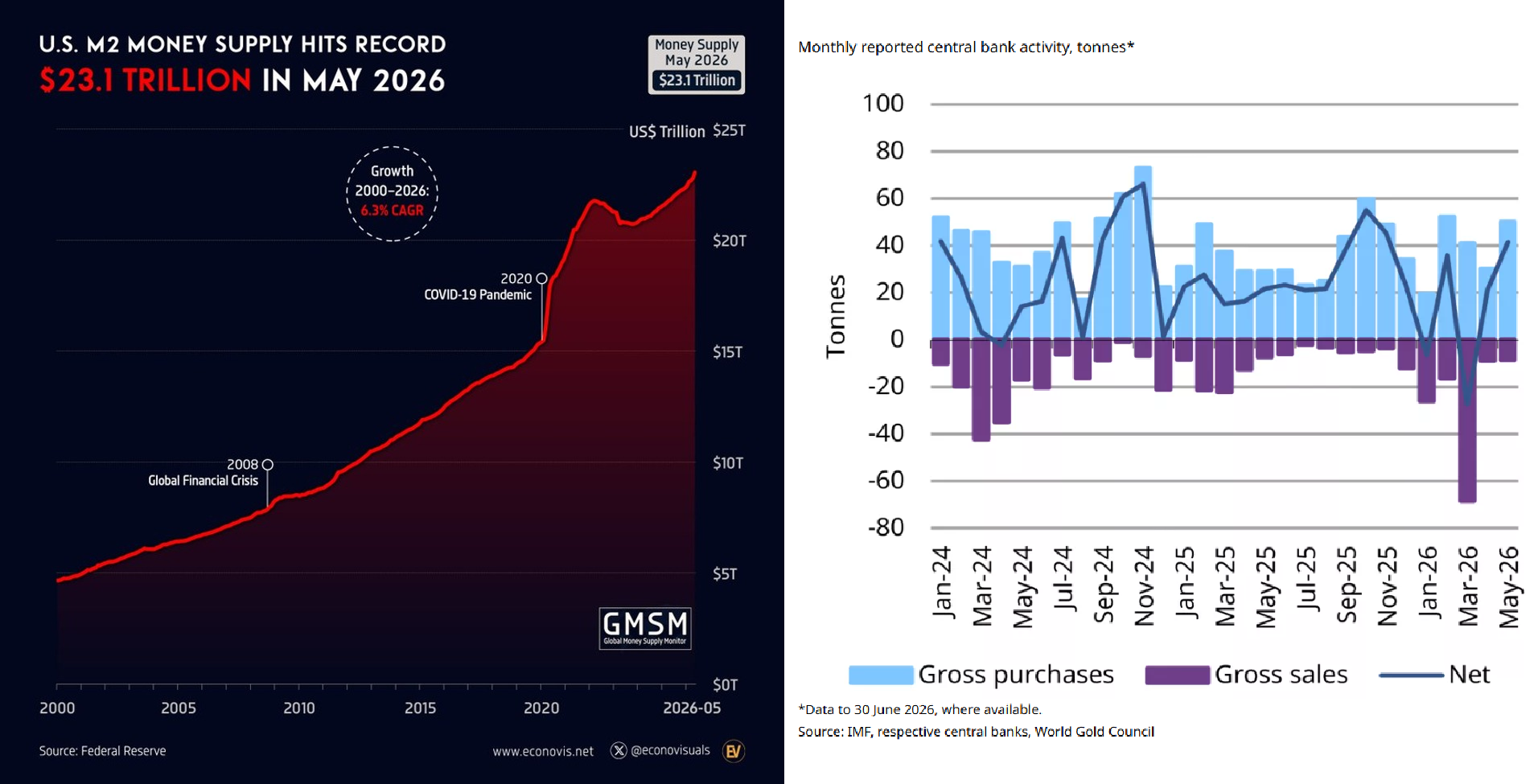

Whether gold is at $4,000 or $5,000 (I'd bet more on $5,000 in the medium term), the need for drilling doesn't go away. On top of that, central banks keep buying gold while continuing to print fiat.

Below the macro picture, here's what we have:

Senior mining companies’ exploration budgets for calendar year 2026 have grown by an average of ~35% year over year. Since these clients represent 90% of Foraco’s revenue, this increase provides strong stability and visibility to its revenue base.

Fleet absorption: The continued rise in drilling demand, from both Senior and Junior miners, is expected to keep absorbing available drilling rig capacity across the sector.

Greater geological complexity: Newly discovered deposits are located in remote, hard to access areas. This requires significantly more complex specialized drilling solutions (deep drilling, helicopter portability, high altitude or arctic conditions), which raises barriers to entry in the sector.

This is one of the best picks I have right now. Not only for the upside, but for the catalysts. The cycle momentum, the size and the operating leverage make it one of the best-positioned names for 2026-27.

🛍️Associated British Foods

ABF is the latest addition to the blog, and to my portfolio too. It's a British conglomerate where Primark, generating roughly half of sales, could be worth the group's entire market cap on its own, leaving Grocery, Ingredients, Sugar and Agriculture effectively for free. The announced spinoff is the catalyst that will force the market to value each division separately.

Shortly after the thesis was published, the company reported Q3 FY26 without altering the thesis direction, as expected. Here's the snapshot I posted on X about the retail division.

Retail (Primark)

Q3 FY26 Snapshot: Sales £2,920m (+3% cc). LFL sales (2.2)%.

Drivers: Total growth was driven by new stores contributing +5%, highlighted by a 16% sales jump in the US. Management noted the new Manhattan store got off to an “absolute flyer” creating a strong halo effect. However, US stores in areas with lower brand awareness (like Memphis and Nashville) were “disappointing”, heavily impacted by severe financial pressure on their core Hispanic consumer base. In the UK, LFL sales were flat, but trading bounced back strongly in June. In Europe, LFL sales fell 3.6% driven by weak consumer confidence in Northern Europe and tough competition in France (notably from Kiabi), though Spain performed better.

Outlook: FY26 guidance remains unchanged, targeting an adjusted operating profit margin of ~10%. Management explicitly stated that next year’s tailwinds (favorable FX and reduced markdowns) will be reinvested into price perception and top-line LFL growth, rather than margin expansion.

‘Wait & see’ ideas

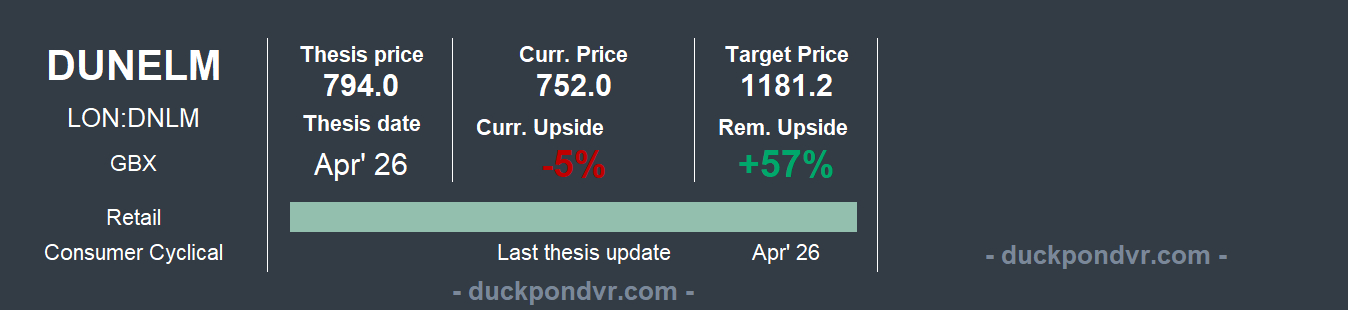

🛏️🛋️🍽️Dunelm

The British homeware retailer is down 21% since the outbreak of the conflict, 29% YTD. This situation is precisely what drew me to this company, which is undoubtedly high quality and has demonstrated consistency in its growth and margins through difficult periods.

That said, the slowdown in Q2 and its confirmation in Q3 did not convince the market, as Dunelm trades on demanding multiples.

Q3 FY26 Results Snapshot

Sales £472m (+2.1%), YTD Sales £1,398m (+3.1%), GM +30bps, Digital 43% (+2ppts)

Drivers: Uncertain consumer environment, customer shift towards discounted products over full price ,Middle East instability (minor direct impact expected).

Outlook: No immediate consumer confidence improvement assumed. FY26 PBT guided to lower end of consensus (£210m-£217m). Accelerating store openings next FY (Kingston-upon-Thames in summer)

As I said, the company has many positive attributes but lacks the margin of safety I look for. You can draw your own conclusions by reading the full thesis. It may offer a good opportunity in the coming months.

Thanks for reading the Value Pond🦆. If you enjoyed it, don’t forget to leave a like 👍subscribe🖊️ and share🔄 it.

DISCLAIMER: All the information provided in this document is purely informative and does not constitute a buying recommendation (according to Spanish Law Article 63 of Law 24/1988, of July 28, on the Stock Market Regulator, and Article 5.1 of Royal Decree 217/2008, of February 15). DuckPond Value Research is not responsible for the use of this information. Before investing in a real account, it is necessary to have the appropriate training or delegate the task to a duly authorized professional.

Reach us on duckpond@duckpondvr.com